What is the fuss?

Since its discovery, gold has captured mankind’s attention. It is the longest form of money known to humans and still holds its weight in the age of digital payments and cryptos.

There is something about the glitter of gold that brings delight to the mind and a desire to possess it. Wars have been fought over gold. Not to mention the special place gold has in gifting during special occasions.

But does Gold retains its shine in the 21st century? It is common nowadays to hear someone multiplying their money in a matter of months. Crypto doubling money and a stock rising 200% in a single year are familiar news headlines. Nowhere is Gold mentioned as giving 2x or 3x returns in a short time.

There is a divide between the schools of thought that still consider Gold an integral part of a wealth creation journey and one that doesn’t. Has Gold started losing its shine?

In this edition, I uncover three lesser-known reasons why Gold can still be a valued asset in your investment portfolio. But first, let’s cover some basics before moving on to these three “shiny” reasons.

Gold Basics: Forms of Investing

When you plan to invest in Gold, do not choose a physical form. Physical gold is okay to gift and wear but not to invest in. It requires maintenance, may get rusted, and is easy to lose or steal.

For investment purposes, go for digital gold assets. These digital gold assets are priced against physical gold, which is stored and maintained by a regulatory body. This is safe, and there is a surety of the returns you will get.

Three common forms of digital Gold are:

(a) Gold Mutual Funds: Example: Nippon India ETF Gold BeES.

(b) Digital Gold: Many platforms, such as Amazon Pay, Tickertape, and Digigold.com, allow the buying and selling of digital Gold.

(c) Sovereign Gold Bond (SGB): My favourite type of digital gold investment, and you will know why by the end of this post.

Now, let’s look into three reasons why investing in gold makes sense.

These three reasons are Returns, Safety, and Stability. I will start with Returns, which is the most interesting and might be an eye-opener.

Reason 1: High Returns

Gold offers high returns, even sometimes matching the stock market index returns. And it hands down beats inflation. Let’s see some numbers for real. (These numbers were taken in February 2024.)

Gold Mutual Funds (81% returns in last five years)

81% returns in 5 years is almost like doubling your money every five years. This is nearly 13% annual CAGR, close to Nifty 50 CAGR in the last five years of 15%.

Digital Gold(86% returns in last five years)

Digital Gold has given 86.23% returns in the last five years. This translates to an annual CAGR of 13.24%, close to Nifty 50 CAGR of 15% in the same period.

Given inflation in India varies between 5 to 7%, Gold comfortably beats inflation.

Gold’s returns also beat bonds (government or corporate), which give returns in the 7–10% range.

Now, let’s look at Sovereign Gold Bonds (SGBs). Since SGB returns are interesting and require some calculation steps, we will go a little deeper to understand them.

Returns from SGBs

First, the reveal. SGBs have given 18% annual CAGR in the past five years (Feb 2019 to Feb 2024).

Wow! It beats stock market index returns and almost doubles your investment in 4 years. I was awestruck when I saw this return, as I never imagined gold giving such multi-bagger returns on investment.

Let’s break down these returns.

Stock Price Appreciation of SGBs

The first leg of returns is the stock price appreciation of SGBs. Yes, SGBs are traded like stocks after being issued. Investors can trade these SGBs in secondary markets such as Kite by Zerodha.

SGBs are given ticker names starting with three letters, SGB, followed by the month and year when they will mature. Each SGB matures in eight years when it can be redeemed in full. Hence, an SGB maturing in October 2025 will have the ticker SGBOCT25. The last two digits are a simple GB. So, the complete ticker of this SGB is SGBOCT25-GB.

As shown below, SGBOCT25-GB has given 132.47% returns in the last five years, which amounts to a CAGR of 15.61%.

Passive Interest Income from SGBs

RBI gives 2.5% fixed interest on the principal amount invested in SGBs. This is credited to your bank account every quarter. This passive interest income is fixed, whether the SGB performs well or poorly in the stock market.

So, the net overall returns from SGBOCT25 are (15.61 + 2.5)% or 18.10% annually.

Will SGBs always give 18% CAGR annual returns?

No, not always. If you look at the 5-year graph of SGB stock price, it grew faster in the initial three years and then slowly in the next two years. Like any stock, SGB rises faster in specific periods and slower in other periods.

SGBs can give zero returns in some years and, in some years, even negative returns.

Macroeconomic factors impact the prices of SGB. One thing is sure: with a limited supply of gold worldwide and increasing demand, SGBs will appreciate over time.

Gold prices usually rise during equity market crashes or financial downturns as investors rush towards safety. Similarly, gold prices may remain flat or decline during bull runs.

Hence, a retail investor can do a monthly SIP in gold and invest in lumpsum when gold prices decline or have stagnated for quite a while.

Now, onto the other two reasons that make investing in Gold attractive.

Reason 2: Safety

Gold is a safe asset class. They will not evaporate your wealth overnight. Let me explain by comparing gold with other investable assets.

Equity

When you invest in equity, you are investing in a company. What if the company becomes outdated? What if it offers products or services that are no longer in demand or better alternatives are available elsewhere? The company’s revenue and related stock price will decline.

Gold does not have this issue. Gold is a commodity and will always be in demand.

Another risk in equities is management risk. What if a company’s management is caught doing fraud? The company and its stock will tank. For example, the Satyam IT scam erased the entire shareholder value of this company. With Gold, this will not happen as it’s not a company managed by executives.

Yes, there can be tinkering in buying or selling physical gold. However, as we are dealing with digital forms of gold validated and managed by the RBI on behalf of the Government of India, there is little to no risk.

Bonds

Corporate or government bonds have low risk as well. Some companies, occasionally, can default on the loans they have taken. Hence, it is advisable to not invest in a single company bond but in a debt mutual fund.

Debt mutual funds distribute invested money across multiple individual bonds, distributing the risk.

Hence, individual bonds are riskier than gold. Debt mutual funds are low-risk.

Crypto

Cryptos are risky and highly volatile. Many crypto trades are based on speculation and social media chatter, making them riskier than gold, bonds, and equity.

Many cryptocurrencies, such as FTX and Luna, have crashed to near-zero value and have not recovered. Cases of fraud have also been reported.

Until cryptocurrencies are regulated and their real-world applications become prevalent, cryptos will remain a risky investment.

Interestingly, Bitcoin, the first cryptocurrency and often the representative of the crypto world, is frequently compared to gold: it has a limited supply over its lifetime and increasing demand.

As you can see, compared with other similar or higher-return assets, gold is much safer.

Reason 3: Stability

Gold gives stability to your overall investment portfolio. Here is why.

Less volatile

Beta is an indicator of volatility. A value of less than one indicates that the stock is less volatile than the stock market index and vice versa.

Gold prices are less volatile. It has a low beta.

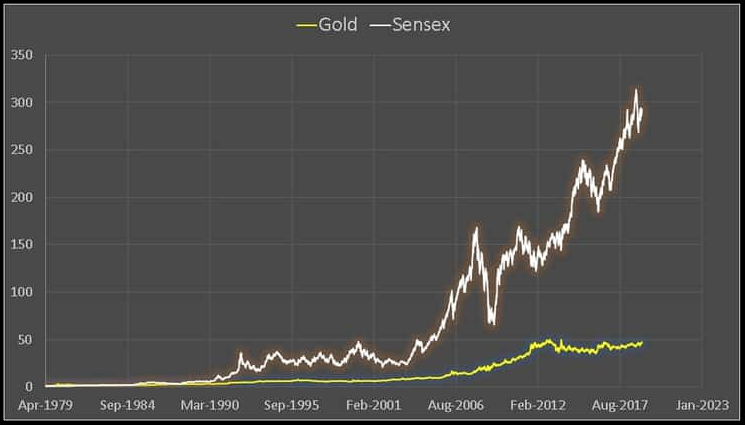

Hedge against Equity

Gold is inversely correlated with equity. This means when equities crash, Gold prices rise. When equity prices rise, gold prices remain flat or go down.

Refer to the last 30 years of Sensex (Indian equity index) and GOld prices as a reference.

Many investors use equity as the primary wealth-compounding machine, and rightly so. However, hedging against equity is advisable, as it will limit the downside during an economic crash.

When will the next economic crash come? Well, no one knows. If people knew, corrective measures would be taken to prevent the crash. However, typically, an economic crash is observed once a decade. A crash can occur because of war, failure of banks or financial enterprises, excessive debt, civil unrest, pandemic, etc.

During a crash, the equity part of your portfolio may tank. However, the gold part of your portfolio will remain flat or increase, thus balancing out the negative impact of the crash.

Bonus: Tips to make higher returns from Investing in Gold

Tip 1: Buy SGBs in the Secondary Market

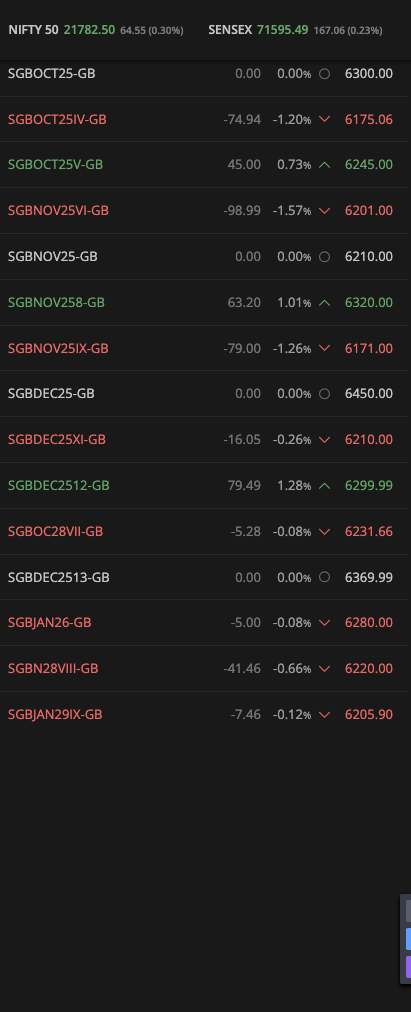

SGB prices in the secondary market are driven by greed and fear. Thus, you may take advantage of the stock market’s mispricing of SGBs. As of February 2024, the same gram of gold is valued differently in different SGBs.

As you can see below, one unit of SGB, which equals 1 gram of gold, varies widely across different SGBs. They range from as low as INR 6,171 to as high as INR 6,450, a spread of 4.5%

Thus, you can get a 5% discount on SGBs in the secondary market. The liquidity of SGBs in the secondary market is not high as of the time of this writing. However, the liquidity is expected to increase as more retail investors get involved.

Tip 2: Hold SGBs longer to pay Low or No Income Tax

Yes, you heard it right. You can have all the gains from SGBs to yourself and not pay a single penny in taxes.

How? By holding an SGB issue till maturity (eight years). If redeemed on maturity, investors pay zero income tax on the gains made from SGBs.

Also, if you hold onto SGBs for three years, you pay a long-term capital gain tax of 20% with indexation benefit. Indexation benefit gives a considerable discount on the final tax you will pay.

Think of it like this: indexation will only calculate tax after considering inflation. Only the gains you made over and above inflation are eligible for tax calculation. This feature lets you pay very little tax on SGBs if held for three years or more.

The takeaway of tip 2 is to invest in SGBs for a long time. Do not park your emergency cash in gold. There are other better-suited investment instruments for parking emergency cash.

Parting Thoughts

The allure of gold is lower among retail investors due to less media coverage. Media articles are ripe with get-rich-quick stocks and related ideas.

Gold is a patient investors’ game. It is a typical buy-and-forget type of asset that can create generational wealth.

Allocating how much gold to your portfolio is a personal choice. At least 10% can be allocated to have a balanced portfolio with less volatility.

Over time, you can increase this allocation as you understand how and when to invest in gold.

I hope this edition threw some “shine” on gold as an investment asset.

How do you invest in Gold? Do share in the comments below.

Disclaimer: This post is not financial advice. I present my views from my experience. Please do your research before investing.