What is the fuss?

The concept of Index Funds has existed since the 1970s, when the “Efficient Market Hypothesis” was developed. Index means tracking a certain stock market index, which is a collection of a number of stocks forming the index.

John Bogle, often called the father of Index Investing, founded the Vanguard Group and launched the first index fund in 1976.

Most actively managed funds in the US have been unable to beat the index. This fact is slowly sinking in, and the FIRE movement in the USA primarily focuses on investing via the index to become financially free.

Investing in index funds offers multiple benefits, including higher returns and low costs.

But what does the story of Index funds look like in India?

Well, it is mixed, and most top actively managed mutual funds in India consistently beat the Indian stock market index funds over a 5+ year period.

But why is that?

In this post, I share six reasons why the Indian actively managed mutual funds outperform index funds and why they might continue to do so in the near future.

We will first compare the performance of the Indian index and actively managed funds and then examine the reasons for the differences.

Note 1: For simplicity, I will focus on large-cap, mid-cap, and small-cap funds, which are the most common equity mutual funds in India.

Note 2: All numbers in this post are taken as of July 2024.

Note 3: I will compare returns over five years. Comparing short-term returns (3 months/ 6 months/ 12 months) does not make sense, as equity investment is a long-term game.

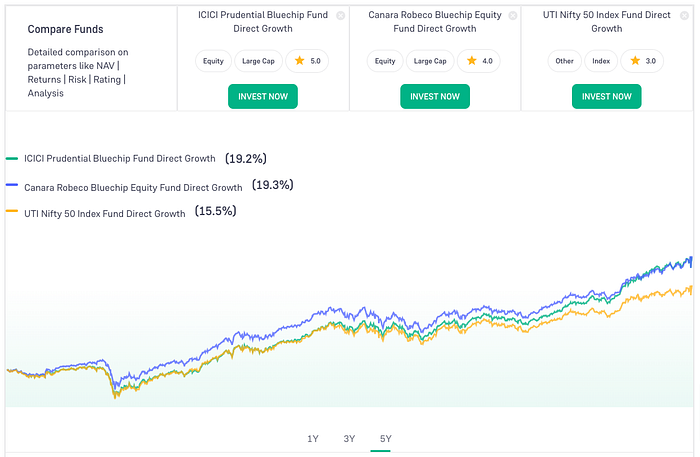

Large Cap Funds vs Large Cap Index

Actively managed large-cap mutual funds are called large-cap funds or blue-chip mutual funds.

I will compare these actively managed large-cap funds with the Nifty 50 Index, which comprises the top 50 largest companies listed on the National Stock Exchange (NSE).

Below, you see that two actively managed large-cap funds, ICICI Bluechip Fund and Canara Robeco Bluechip Fund, outperform the Nifty 50 index fund by a wide margin over a 5-year period.

These actively managed large-cap funds give an absolute ~4% annual CAGR higher than the large-cap index fund itself.

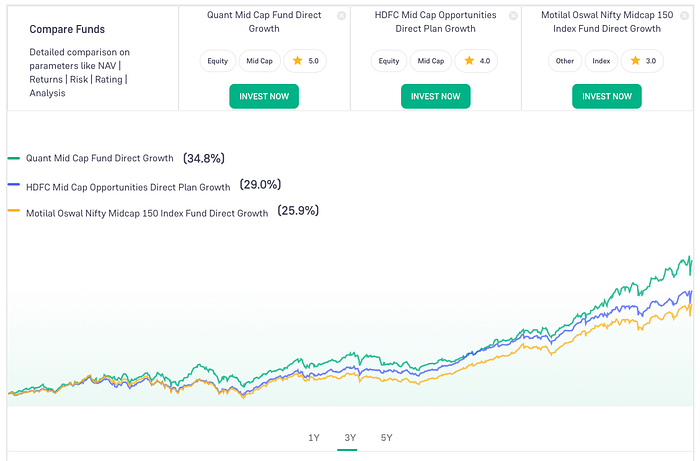

Mid-Cap Funds vs. Mid-Cap Index

Actively managed mid-cap mutual funds are called mid-cap funds or mid-cap opportunities funds.

These mid-cap funds try to beat the Nifty MidCap 150 index, a collection of the 150 largest mid-cap companies ranked 100th to 250th in terms of overall market capitalisation.

As we see below, two popular actively managed mid-cap funds (Quant Mid Cap and HDFC Mid Cap funds) have beaten the oldest mid-cap Index fund in India, Motilal Oswal’s Nifty Midcap 150 Index fund.

Note: MidCap Index funds were recently launched; they do not have a five-year or longer history. Hence, I am comparing the CAGR returns from the last three years.

These actively managed mid-cap funds give an absolute 3–9% annual CAGR higher than the mid-cap index fund itself.

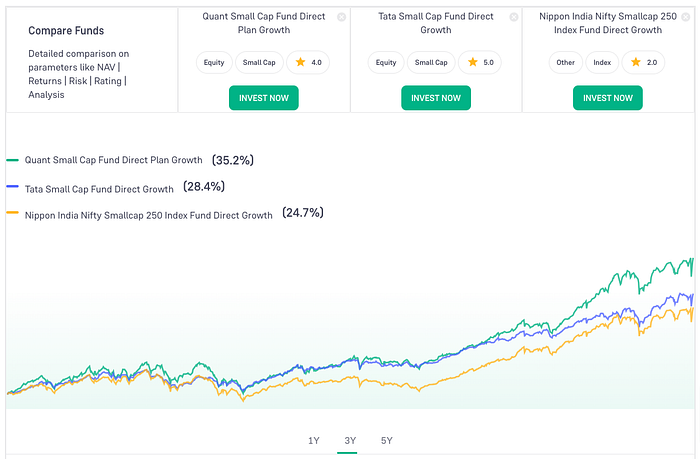

Small-Cap Funds vs. Small-Cap Index

Actively managed small-cap funds in India try to beat the Nifty SmallCap 250 index. This index is a collection of the 250 largest small-cap companies ranked 250th to 500th in terms of overall market capitalisation.

As we see below, two popular actively managed small-cap funds (Quant Small Cap and Tata Small Cap funds) have beaten India’s Small Cap Index fund, the Nippon India Smallcap 250 index fund.

Note: Small-cap index funds were recently launched; they do not have a five-year or longer history. Hence, I am comparing the CAGR returns from the last three years.

These actively managed small-cap funds give an absolute 4–10% annual CAGR higher than the small-cap index fund itself.

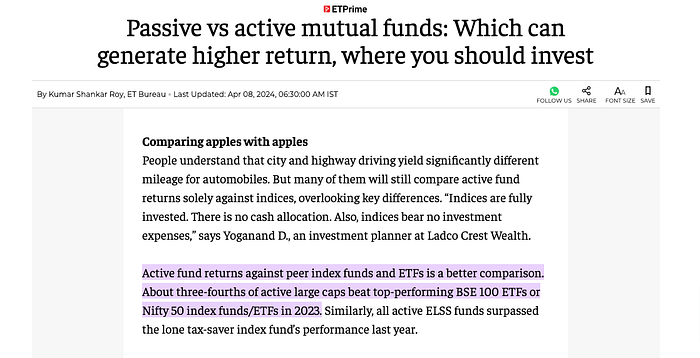

Some actively managed funds in India may underperform index funds. However, as the 2024 article in the Economic Times below mentions, most of the largest actively managed funds outperform index funds.

Now, having seen actively managed funds outperform index funds, it might seem counterintuitive at first. Why would this happen in the Indian Stock market but not in the US Stock Market?

Well, here are six reasons why.

Reason 1: Exclude companies with Governance Issues

You will notice several reasons in this post for excluding low-quality stocks. Index funds are mandated to track the index; hence, they cannot exclude a stock even if the fund manager knows the company behind the stock is not well-managed.

One of the top reasons active funds do better is their freedom to avoid companies with governance issues.

Companies with poor governance might not create stakeholder value in the long term. These companies may show high volatility and use shady methods to juice up their stock price to benefit them.

For example, actively managed large-cap funds mentioned above, ICICI BlueChip fund and Canara Robeco BlueChip fund, do not own Adani Group stocks.

Even though two Adani Group companies, Adani Ports and Adani Enterprises, are part of the Nifty 50 index, these actively managed funds do not own either of these stocks.

In 2023, Hindenberg published a detailed report on the Adani group, claiming stock manipulation and accounting fraud in the Adani Group companies. While the investigations are ongoing, this does signal malpractice in the company.

There can be more reasons behind staying away from Adani companies. The mutual funds might be awaiting the final verdict of the investigation. Or that the free float in Adani companies is very low, making it a highly volatile stock, or that the now-ruling government favours the group and might face headwinds once the government changes.

Whatever the reason, the freedom to stay away from doubtful companies with poor governance is an advantage that active funds have.

It is important to note the difference between the US and Indian listed companies. Most of the listed companies in India are family-run businesses, and some might have governance issues that need to be identified and excluded from one’s portfolio.

In the US, many listed companies are professionally managed, and corporate governance issues have become less prevalent in recent times.

Reason 2: Exclude Companies with short-term Headwinds

All companies undergo an upcycle and a downcycle, but the time period of these cycles may differ. Some cycles last a couple of years, whereas in some industries, such as real estate, they can be decades long.

What do you do with an industry that is undergoing a downcycle? Well, you can avoid these companies and put more of your money into companies undergoing an upcycle.

As an index fund, you don’t have this freedom. However, as an active mutual fund manager, you can exclude companies on a certain downcycle until cycle reversal signs are clear and evident.

Example: IT Sector

The Indian IT sector is experiencing a temporary headwind in 2023 and early 2024. It started in late 2022 and will likely end with interest cuts worldwide, primarily in the US and India. These rate cuts will spur corporate capex, revive dormant IT projects, and enable global companies to make new digital investments.

Actively managed large-cap funds have reduced or cut exposure to IT large-cap stocks during this slower down cycle to reduce exposure to the IT sector.

TCS (Tata Consultancy Services), which has a weightage of 4% in the NIfty 50 index, has just a weightage of 0.4% in the ICICI Blue Chip fund and 0.8% in the Canara Robeco Bluechip fund.

The above actively managed large-cap mutual funds exclude LTIMindtree, which has 0.5% weightage in the Nifty 50 index. Apart from the IT sector downcycle, LTIMindtree is stressed from the recent merger between LTI and MIindtree, followed by many CXOs’ exits.

This gives actively managed funds an advantage: they can ride the positive wave of industry upcycles while avoiding or reducing the drag of industries in a certain downcycle.

Note that it is not about timing the market but avoiding certain industry cycles. Entering or exiting these cycles cannot be perfect. However, as these cycles last more than a year, the freedom to identify and stay away from downcycles rewards these actively managed funds.

Reason 3: Stay within one’s Circle of Competence

Investing veteran Mr Warren Buffet popularised the concept of staying within one’s circle of competence. It means investing in businesses you understand and avoiding those you do not know about.

The intent behind this is to do well in what you understand well instead of dabbling in stuff you do not know. Dabbling for the sake of learning is ok, but allocating a significant chunk of your wealth into an area in which you do not have competence is not a sound decision.

Every fund manager has a circle of competence. Some are good at picking financial stocks, some at picking manufacturing companies, some have a keen know-how of the chemicals industry, and so on.

Fund managers of actively managed funds have the freedom to exercise their circle of competence and keep a distance from industries they do not understand or are less fond of, so to speak.

Two industries often fall into the latter categories: Metals and Public Sector Undertakings (PSUs). Metals are widely cyclical, less-moated businesses with fewer price controls (traded as commodities). Similarly, PSU companies have had a weak track record, as their main aim is social welfare and generating income for the government in the form of dividends.

Example 1: JSW Steel and Tata Steel are part of the Nifty 50 index (large-cap index). However, neither of these companies is owned by the two actively managed funds in our comparison above (ICICI Bluechip and Canara Robeco Bluechip funds)

Example 2: PSU stocks such as Coal India, Bharat Petroleum, and ONGC are part of the Nifty 50 Index but are not owned by the Canara Robeco Bluechip fund.

Do note that these actively managed funds can, for some quarters, own PSU companies or Metal stocks. They typically do so when there is a strong visible tailwind in these sectors, driven by market demand or government policies.

Actively managed funds pick stocks to maximise risk-adjusted returns for their investors. Hence, when risk is minimal and rewards are higher in the short to mid-term, these funds take an exception and invest in their less-preferred stocks to ride the wave.

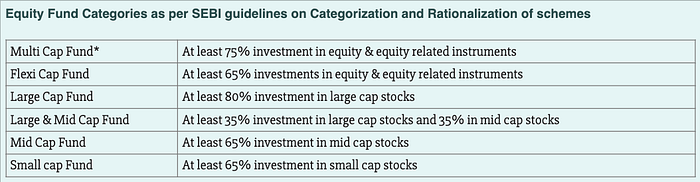

Reason 4: LargeCap funds can invest in SmallCaps, and vice versa

Actively managed mutual funds can take advantage of how regulations define large-cap, mid-cap, and small-cap fund categories.

What definitions? Below are the definitions, as per AMFI (Association of Mutual Funds of India).

Large-Cap Mutual Funds

A large-cap mutual fund has to invest 80% of its assets into large-cap companies. This means it can choose to invest the remaining 20% in mid-caps or small-caps. This gives these large-cap funds an advantage; they can create higher alpha by investing a small portion of their portfolio into faster-growing mid-caps or small-caps.

What is Alpha? Alpha is a metric used to measure the relative overperformance of a stock or fund compared to the index it tracks.

Large-cap fund example: Canara Robeco Bluechip fund has invested 8% of its equity portfolio into mid-cap, high-growth stocks such as CG Power, Cholamandalam Investments, Sona BLW Forgings, Siemens, etc.

Mid-cap Mutual Funds

A mid-cap fund must invest at least 65% of its assets in mid-cap companies. It can invest the remaining part of its portfolio in large-cap or small-cap companies. While investing in large-cap companies can stabilise a portfolio and limit drawdowns during market downturns, investing in high-growth small-cap stocks can boost the alpha of the entire mid-cap fund.

Mid-cap fund example: The HDFC Mid-cap Opportunities fund invests 12% in large-cap stocks (Hindustan Aeronautics Ltd, Bharat Electronics, etc.) and 15% in small-cap stocks (Greenlam Industries, Arvind Ltd., etc.).

Small-cap Mutual Funds

A small-cap fund must invest at least 65% of its assets in small-cap companies. It can invest the remaining part of its portfolio in large-cap or mid-cap companies. Investing in large-cap companies can give a huge stability boost to a small-cap portfolio. Small-cap stocks are small companies, and their prices are highly volatile. They might generate higher returns during market upswings but can also fall like bricks during downturns. Thus, large-cap companies can cushion the fall of a small-cap heavy portfolio, overall improving the return from the portfolio in the long run.

Small-cap fund example: Quant’s Small-cap fund has 16% of its portfolio in two large-cap names: Reliance and Jio Financial Services. This fund has widely outperformed the small-cap index. It is an example of a well-made portfolio mix of large-caps and small-caps, with a 26% overall allocation towards stable, consistent compounding large-cap companies.

As you saw above, actively managed mutual funds use the regulatory definition of a fund category to their advantage. They either add stocks from a different category to increase their alpha (returns) or provide stability to the portfolio, thus reducing drawdowns when they occur.

Reason 5: Sitting on Cash

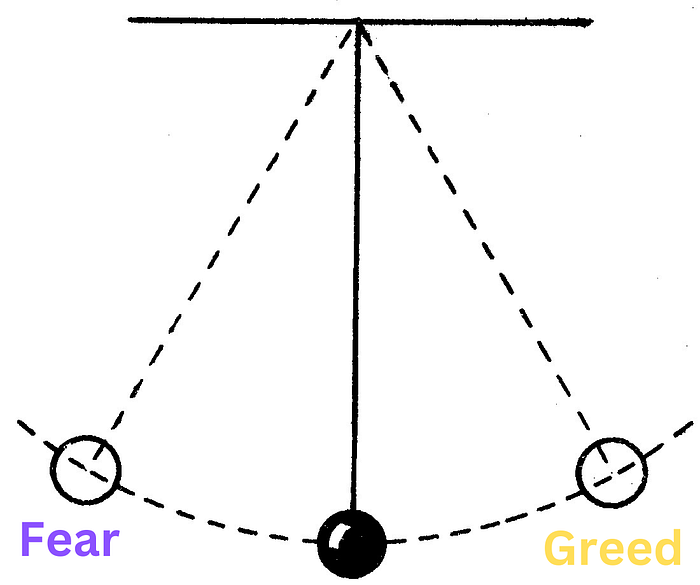

What do you do when the market is extremely overvalued? Well, you might sit it out and not deploy additional capital into the stock market.

The stock market’s mood is like a pendulum, swinging between extremes of fear and greed. When it swings toward extreme greed, bubbles are formed, and stocks start trading at unsustainable valuations.

One thing is certain at this point: the pendulum will swing back, reversing its direction, correcting the market and making valuations reasonable again.

But what if you invested at this point of extreme greed? Well, in the short term, you will lose money. Your investments will fall into loss, and you will have to wait for the next market upcycle to get back into profit. Now, this can take some time, maybe some quarters or even a year. Not good, right?

Mutual fund managers know this. Hence, they take some chips off the table when they see extreme exuberance in the stock market. They sit on cash.

Yes, they allocate some part of the portfolio to cash. In investing, this is also called ‘dry gunpowder’.

Why ‘dry gunpowder’? Well, because this cash is ready to be deployed as soon as the market corrects. It might not cause a “boom” when deployed, but it can be invested in the blink of an eye (well, in a day, maybe).

Actively managed mutual funds sit on cash during times of extreme greed. Some funds always have a certain allocation of cash to use as soon as an exciting opportunity arises.

When greed becomes extreme, these funds increase the cash allocation and wait for reasonable times to return. There is no point in investing at higher valuations when you know the correction is around the corner, and any money invested now will only correct and give short-term loss.

As you can see below, the sample small-cap and mid-cap funds we used in our comparison above have 5% and 8% cash allocations, respectively. Meanwhile, the index fund (UTI Nifty 50 Index fund) has a 0% cash allocation.

Sitting on cash is also a favourite strategy used by veteran investors, some of whom have been able to beat the index. Warren Buffet is the name that comes to mind, whose cash pile investors and news/media track carefully.

Reason 6: The Indian Stock Market is yet to mature

This is a philosophical reason backed by some facts. Going back to where I started this post, in the 1970s, when the Efficient Market Hypothesis came into being, and the Index Fund was born thereafter. The efficient market hypothesis states that it is difficult to outperform the market by picking stocks and timing the market, as the market prices reflect all available information.

This is true to a large extent in a mature stock market such as the USA. However, the Indian stock market has yet to mature to the US level. Some industries in India are not listed (personal help/services, kirana stores, etc.). Many industry sectors (apparel, shoes, etc.) are unorganised, thus not participating in the public markets. Many VC-funded unicorns have yet to do an IPO (Urban Company, Oyo Rooms, etc.).

Once the stock market becomes a truer representative of the businesses that operate in India, outperformance by stock picking will become difficult.

I believe in Index Funds, though I think their time in India has not yet arrived. Don’t get me wrong; Indian Index funds do give decent returns. However, if I can get better returns by investing in actively managed funds and not paying a lot more (reasonable expense ratios), I am good.

Parting Thoughts

Since I read John Bogle’s book The Little Book on Common Sense Investing, I have intended to invest in Index Funds. The book makes sense and has ample data to prove that Index Funds are safe, rewarding, and less expensive. However, after four years of contemplation, I have let data make the decision for me. For now, I am sticking with actively managed equity funds in the Indian stock market.

I do invest in US ETFs (Index tracking Funds traded as stocks on the market). In fact, 100% of my US equity portfolio is via ETFs, which track US Stock market indices. And my US portfolio has performed well.

Index funds and Actively managed funds can coexist in your portfolio. Over time, you can make up your mind about which funds to increase allocation to and by how much.

The Indian Index funds market has been picking up pace, which is a good sign. Many mutual fund houses are launching variations of index funds, combining them with factors such as momentum, quality, low volatility, etc.

The National Stock Exchange also keeps coming up with new indices to track emerging sunrise sectors. Some examples are the Nifty EV & New Age Automotive Index and the Nifty India Tourism Index.

I am hopeful and look forward to chilled-out, passive-style investing in India in the near future, which I believe would be a good match for a future retired me 🙂.

Do you invest in Indian Mutual Funds? Which type do you prefer, active-managed or passive index funds? Please share in the comments.

Disclaimer: I have shared my investing experience in this post. This is not financial advice. Please do your research before investing.