This Indian API Manufacturer looks ripe for accumulating in 2023

This post is part of quarterly earnings discussion series I write. I share my analysis, and future growth prospects of listed companies. This is not a buy/sell recommendation. Please do your own research before investing.

First, some context

Laurus labs posted a lukewarm Q3 FY 23 results on 30th Jan 2023. The markets did not like the results, and the earnings missed estimates. Laurus Labs stock price fell by 9% on the day the results were announced.

Laurus labs has been hailing the ARV drug for HIV as its champion to drive growth for the past 3–4 years. However, this story seems to be over now. Not only is there intense competition, but also price erosion. Laurus Labs has corrected 36% in the past 1 year. From highs of INR 626/-, it is trading at INR 335/- in Feb’23. Its PE has downrated in the last 1 year from 42 to a low of 20. The company’s stock price chart looks like a falling knife, and has left investors bleeding and exiting in disappointment.

So, why am I being positive on this stock now? You will find out soon. Lets start with the businesses of Laurus Labs, followed by decoding its Q3 FY 23 results, and then studying its future growth strategy.

The Four Pillars of Laurus’ Business

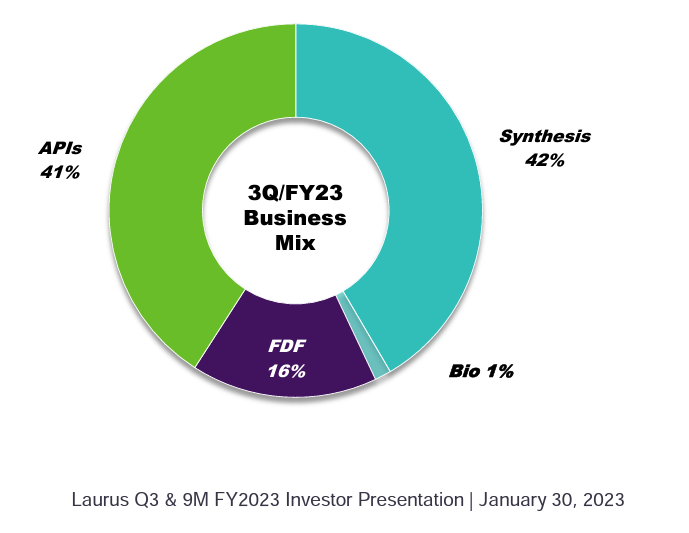

Pillar 1: Formulations (FDF)

Formulations means to combine different chemicals, including the main active drug, to make the final medicine. FDF stands for Finished Dosage Form. This typically contributes 40% of topline revenue, led by ARV formulation business (FY 22 reference).

Pillar 2: APIs

API stands for Active Pharmaceutical Ingredients. Laurus manufactures around 60 APIs for generic drugs. This vertical typically contributes to another 40% of topline revenue (FY 22 reference).

Pillar 3: CDMO (Synthesis)

CDMO stands for Contract Development and Manufacturing Organization. Big pharma companies find it easier, and cost efficient to outsource drug development and manufacturing to low cost countries such as India. CDMO is also referred to as Custom Synthesis, or just Synthesis. This business contributes to 19% of topline revenue for Laurus (FY 22 reference).

Pillar 4: Bio

Laurus Bio is the new kid on the block. It is similar to CDMO. CDMO (Synthesis) is for chemicals, whereas Bio is for bio similar products. Example: Animal Origin Free (AOF) protein. I won’t take more examples, as each new product comes with its own acronym :-). Bio contributes a small portion to topline revenue, typically 1–2%.

Laurus Labs Q3 FY 22 – Highlights and Lowlights

Highlights – Q3 FY 23

[+] Pillar 2 – Generic API business grew 49% YoY (year over year), but declined 7% QoQ (Q3 FY 23 vs Q2 Fy 22). Onco API business de-grew by 13%, dragging down the API business sequentially QoQ.

[+] Pillar 3 – CDMO business grew by 210% YoY, though it declined 11% QoQ.

Lowlights – Q3 FY 23

[-] Pillar 1 – Formulations business, declined 33% YoY, driven by soft ARV demand and weak price.

[-] Bio business declined 12% YoY, and 19% QoQ. This is driven by unscheduled downtime in Q3 FY 23.

[-] High Margin ARV business, which contributed to >80% to topline (Formulations + API business), now only contributes 60%.

Q3 FY 23 looks more bad than good so far, and you won’t be wrong. Now, lets look at future growth guidance, where things start looking interesting.

Future Guidance

ARV Drug impact to reduce

Laurus has been selected as “panel supplier” for ARV drugs from 2023–2025. Supplies to begin Q1 FY 24 onwards. Volume and price point has not been disclosed. However, it is expected to be at a lower price vs historically. At least the volumes from ARV drugs will come back Apr’23 onwards.

Expansion of CDMO on track

CDMO dedicated R&D center and two manufacturing units are on track, and will become operational in FY 24. CDMO is pegged as the new growth lever for the company in coming years.

Capex to drive API Business growth

Laurus has solid pipeline of API filings in US and Canada (36 ANDAs and 75 DMFs). Greenfield expansion in Vizag (Unit 7 and Unit 8) is on track to be completed by FY 25 (2 years from now).

Margins expected to recover

Q3 FY 23 saw slight dip in operating margins from 28% in Q2 FY 22 to 26% in Q3 FY 23. This will recover to 28–30% in future quarters. As per CEO Mr Chava, newer and faster growing business verticals have higher margin, which will negate any margin erosion in other verticals such as ARV.

Bio Business Capex

R3 plant brownfield expansion to start. Land acquisition near Mysore will commence shortly for the same. No timelines given for date of commissioning/revenue generation. As we are in land acquisition phase, which is typically followed by construction, then test batches, then regulatory clearance etc, I would say it will take 2-3 years for this capex to meaningfully impact Laurus’ Bio business pillar.

What augers well for Laurus?

Capex plan on track

Capex plan and progress is on track, which shows good execution of the management. There are no delays noted in the last 3 quarters. Also, the capex will not increase debt to equity of the company, which is a good sign.

R&D Focus

Laurus has a good R&D focus, with 4-5% of revenue spent on R&D. The API filings of the company (ANDAs and DMFs) have been consistently increasing year over year. This gives confidence in future revenue growth for the company, once these filings get approved and start contributing to revenues.

Fair Valuations with Margin of Safety

With almost 40% correction in Laurus’ stock price, it is now trading at fair valuations of PE 20. Historical PE of the company has been 36. Hence, there is good margin of safety in 2023.

Do note that Laurus can fall further given the weak market sentiment. I think that the worst is over for the company, and the company is going into neglected zone. This neglected zone is the right zone to start accumulating, and something that I plan to do.

I do not think Laurus will give positive returns in 2023, hence short term investors can avoid this company. Long term investors with 3–5 year investment horizon, can consider Laurus for investment, as the next boost in revenue is expected FY 25 onwards.

Parting Thoughts

Investors should start looking at a fundamentally strong company, when the stock market starts neglecting it. Laurus labs is in that spot. Its ARV growth story panned out well over the past 3 years. But that story is waning away now. The new story of CDMO, API, and its fledgling Bio vertical will throw light on the next growth runway for Laurus.

Investing in Laurus when it is down might seem like contrarian investing. You would be going in the opposite direction of all other investors. However, with your research on the fundamental strength of a company, its history, and committed management – sometimes the riskier bets give the highest rewards.

Some key things investors should track, and watch out for in 2023 are: (a) Capex progress (b) Margins (c) CDMO and API business growth. Any disruption to the future growth plans should be closely evaluated. Potential risks to the company are elevated raw material prices, fumble in regulatory clearance of manufacturing facilities, uncertain demand driven by weak macro economic situation, and delays in Capex plans.

There is no strong guidance for stellar growth in FY 24. Laurus’ CEO Mr Chava, in an interview to Bloomberg, said that 2023 will be a year of consolidation. One can interpret this as, 2023 will be boring at best, for Laurus labs. The next engine of growth is expected to start roaring 2024 onwards. This will driven by CDMO capex, and R&D driven API business. Bio business will mostly be flattish, and may seen an uptick once the brownfield expansion in Mysore starts contributing to the topline.

Though no one can be sure of a company’s future, Laurus Labs is one API manufacturer to watch out for in 2023. Long term investors can consider accumulating this stock in a staggered manner in 2023.

Happy Investing!

Disclaimer: DYOR before investing.