What is the Fuss?

Tata Chemicals announced its Q4 FY 23 earnings on 3rd May, 2023. This company has historically traded at a low Price to Earnings (PE) multiple of 8–10. After de-merging its FMCG business into another listed company, Tata Consumer Products, Tata Chemicals has embarked on a journey to tap into emerging trends such as solar energy. This post covers key highlights from Q4 FY 23 earnings call, and reasons why this stock should be on investors’ radar.

The Company — Tata Chemicals

Hearing the company name, Tata Chemicals, people might think of Tata Salt, desh ka namak. However, this is not entirely accurate. Tata Salt brand was transferred in 2020 to the FMCG company Tata Consumer Products. Post this, Tata Chemicals is left with three key business verticals — Soda Ash, Sodium Bicarbonate, and Salt (industrial usage). These three business lines are called Basic Chemistry Products.

Some might be surprised to know that Tata Chemicals also has an agrochemical arm, via a fully owned subsidiary — Rallis. Rallis is listed separately on the stock market.

Apart from Basic Chemistry (reflected in standalone financials), and Rallis (reflected in consolidated financials of the company), Tata Chemicals has a small bromine / chlorine derived products plant. However this is too small to be discussed in the company research. Company has not revealed plans to expand on bromine/chlorine business, hence I will leave this out for now.

Global Reach

Tata Chemicals plants are spread across the world. It has presence in the US, Europe, India, South Africa and Singapore. The company aims to reduce logistics costs by strategically setting up plants nearer to consumer market, or nearer to ports.

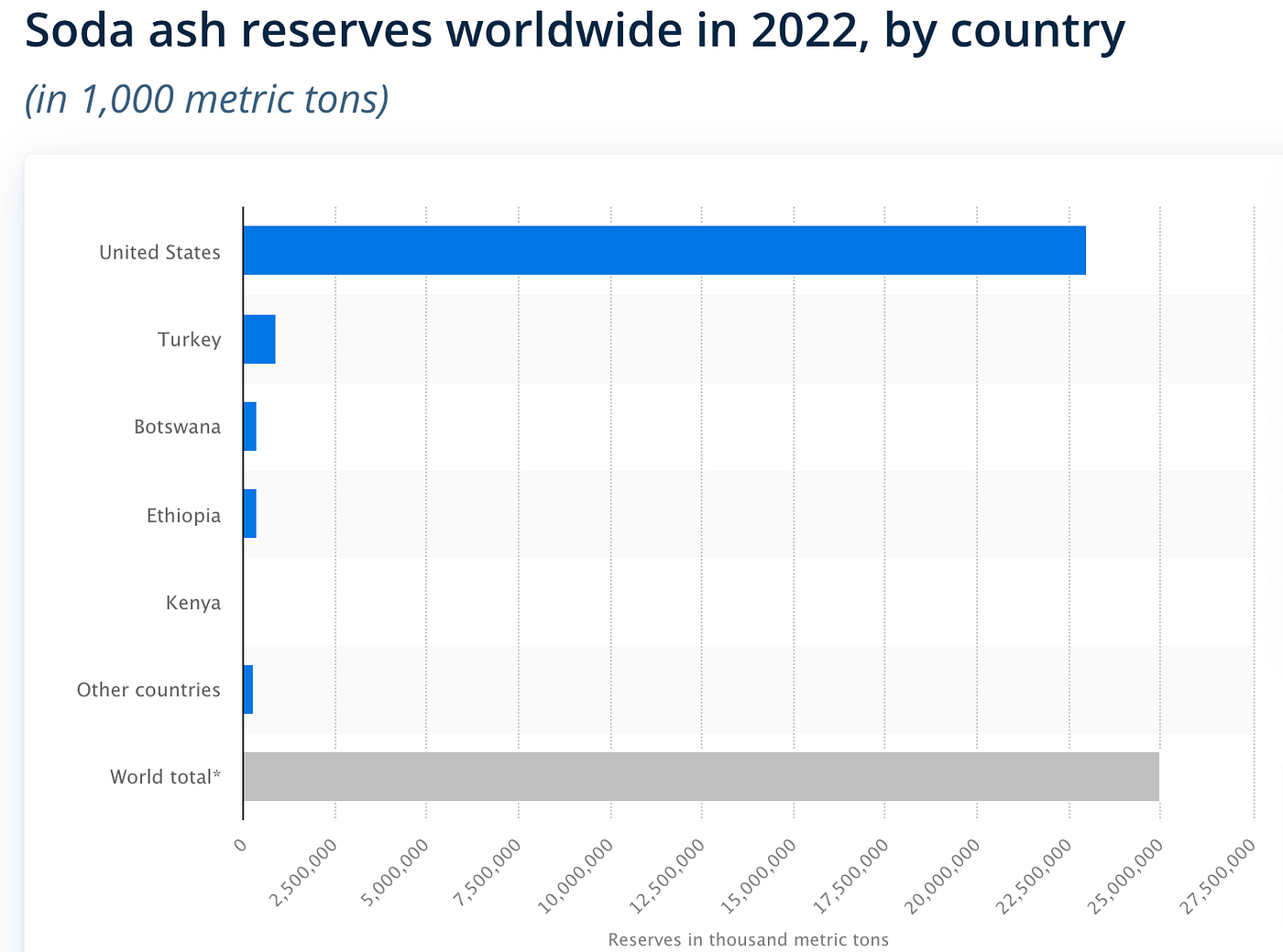

US has the largest natural reserves of Soda Ash in the world, as shown below. Tata Chemicals targets natural source of soda ash, vs synthetic soda ash manufacturing, as the former is preferred by its customers.

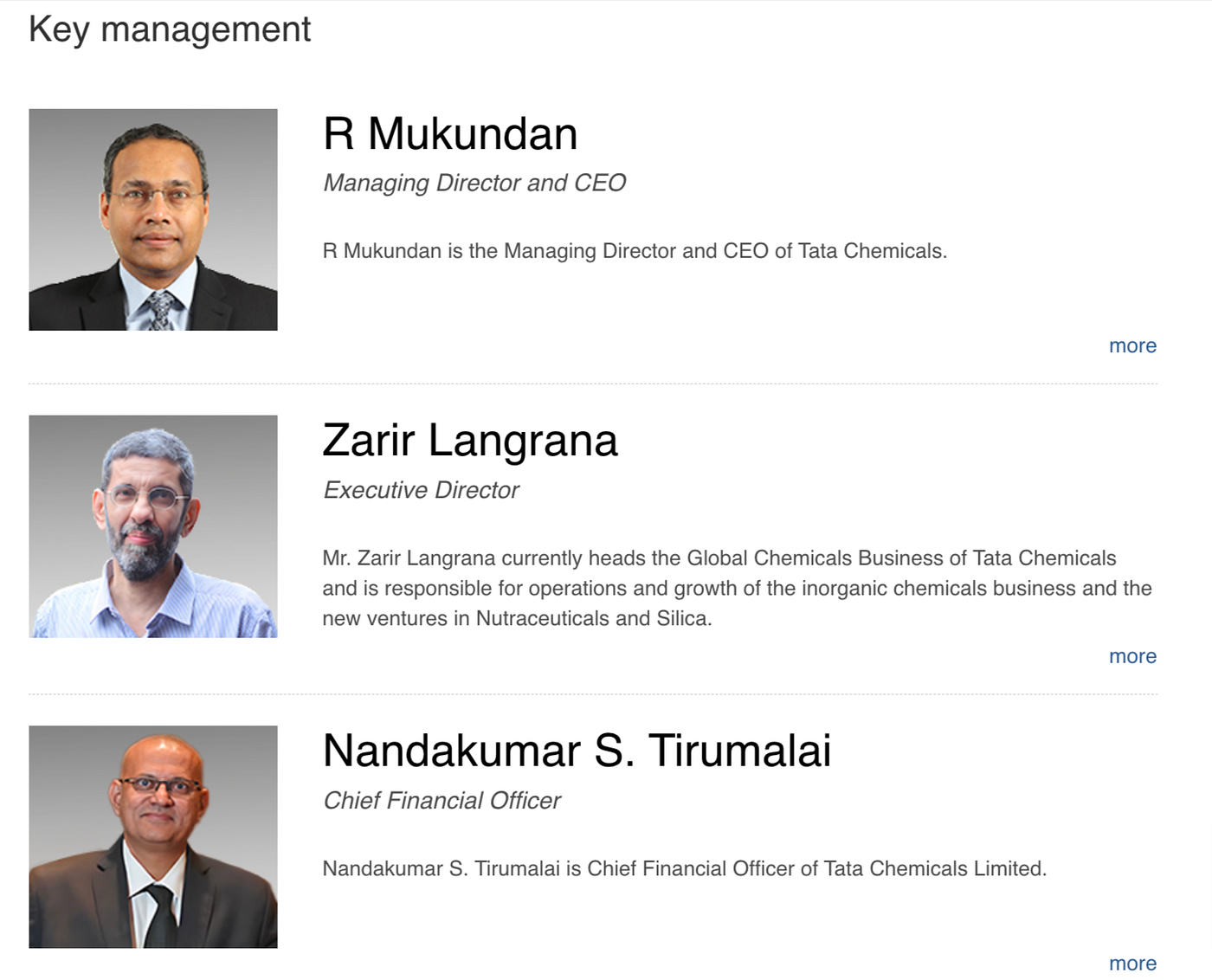

Experienced Management

Tata Chemicals leadership team comprises of tenured employees, who have spent more than a decade each in the Tata Group companies. Its CEO, Mr R Mukundan, is a IIT Roorkee graduate. Global Business head Mr Zarir is XLRI Jamshedpur graduate. CFO, MR Nandkumar is a chartered accountant.

Management with long experience in the industry, and within Tata group, gives confidence of their commitment. Tata group is known for high bar on corporate governance, and is a brand trusted by many.

Given that Tata Chemicals has a sound business, strong management, and a global reach, one might wonder why this stock has not given stellar returns to its investors. In the last 1 year (May 2022 to May 2023), Tata Chemicals stock has given -3.7% returns, vs 12% returns given by Nifty 50. Following section covers some of the reason for low returns given by this stock, which will connect to the Q4 FY 23 highlights and the reasons why this stock is turning corners.

Reasons for Average Stock Performance of Tata Chemicals

Reason 1: Price Taker, and not a Price Maker

This simply means that Tata Chemicals is not a price maker of its products. It is unable to demand a price for soda ash, sodium bicarbonate etc. Instead, soda ash prices are set by the market. If a global competitor increases supply of soda ash, Tata Chemicals will have to reduce its soda ash price to remain competitive in the market.

One such instance occurred recently in Apr’23, when China announced increase in capacity of its soda-ash manufacturing in inner Mongolia region (article here). This led to Tata Chemicals reducing its soda ash prices to offer competitive prices to customers given the increase in supply.

I do not think there is a short term mitigation of this limitation. Over long term, it is better if Tata Chemicals diversifies and grows it other business verticals to prevent over-dependency on soda ash. As long as soda ash is considered, Tata Chemicals is already among the top 5 suppliers in the world, and is on track to expand its capacities in coming years to maintain its leadership position.

Reason 2: Underperformance of Rallis

Rallis, a fully owned subsidiary of Tata Chemicals, has underperformed vs other agrochemical companies. There are some glaring mistakes in Rallis’s past, such as its investment in cotton seeds which did not generate returns due to farmers’ preference for cheaper cotton seeds available to them. Similarly, their millet seeds were not preferred by farmers, and the R&D cost and inventory built up had to be written off. These instances show lack of expertise of Rallis management in cropcare and seed industry.

Tata Chemicals remains bullish on the Rallis story, and banking on its turnaround by 2025.

Having covered the not so exciting past of Tata Chemicals, time to know what is turning me positive on the company now.

Future Growth Levers (FY 2024 onwards)

Lever 1: Opening up of Demand

China is opening up after a prolonged covid lockdown. This has led to resurgence of demand of dense soda ash used in container glass industry. Apart from China, demand in the US is expected to remain strong going forward.

Lever 2: Emerging Solar Industry

Solar is one of the main renewable sources of energy mankind is bullish about. Rise in electric vehicles, increase in solar roof installations, and massive funding of emerging solar technology companies give a strong signal in this direction.

Soda ash is an essential raw material requirement in solar glass plants. With many countries, including India, committing to certain gigawatt (GW) of solar energy production in coming years, an emerging demand of soda ash and sodium bicarbonate is expected starting FY 24.

In Q4 FY23 concall, Tata Chemicals leadership referred to India’s commitment to add 100 GW of solar power by 2025. Each GW of solar power requires 1 million ton of soda ash. A large part of this domestic demand is expected to be fulfilled by Tata Chemicals, the largest producer of soda ash in India.

Lever 3: Reduction in debt

High debt is an overhang on a company’s stock price. Rising interest rate environment further puts pressure on the bottom line of a company with high debt. High debt companies get lower valuations from the stock market, commensurate with the risk associated with debt.

In short, debt is bad. Tata Chemicals is reducing debt, which is good.

The company has overdelivered on its debt reduction targets in the past. In FY 23 ending March 2023, Tata Chemicals paid debt of USD 150 million, against a commitment of paying off USD 100 million. This instills confidence in their forward looking commitment of reducing debt by USD 200 million in FY 24. Their current debt to equity is 0.32, which should reduce to less than 0.2 by FY 24 end.

Parting Thoughts

Tata Chemicals is a bag of good management, selling an average margin product, in a competitive global industry growing 6% annually. The new sunrise sectors of solar energy can act as growth catalyst. What makes me optimistic about this Tata Group company is their management, and their history of walking the talk. If they are able to drive the three levers mentioned in earlier section, it might result in a re-rating of the stock, and generate above average returns for its investors.

Key risks to watch out for is changes in competitive landscape, adverse macro environment, and reversal in soda ash demand cycle.

In the worse case scenario, Tata Chemicals will remain to be a slow growing stock, giving 8% annual returns in price appreciation, and 2% dividends, amounting to overall 10% annual returns. This is not bad either :-). Given the limited downside, and potentially higher upside, Tata Chemicals is a strong candidate to keep on your investment radar.

Disclaimer: I am not a SEBI registered advisor. Please do your own research before investing. Consider subscribing to my weekly email newsletter here, to receive subscriber only info on the Indian Stock Market.