Company Description

Rallis India, a Tata Group company Group Co., has a history of over 150 years. The company is into manufacturing of agrochemicals and is present across the value chain of agriculture inputs – from seeds to organic plant growth nutrients.

Catchphrase of the Company

Mission

Rallis aspires to be amongst top three leading enterprises by 2026 in the chosen areas within farm inputs and chemistry led businesses.

Technical Analysis – Poor Performer

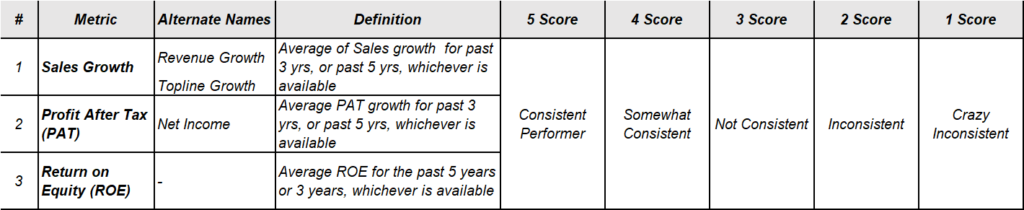

Consistency: Somewhat Consistent (4 / 5)

Rallis Consistency: Rallis’s consistency is average. Revenue has consistently grown at 11% CAGR for the past 5 years. ROE growth rate has been consistent in the last 5 years at 14%. However PAT has been consistent in all but the last year, for the past 5 year period. Hence, overall score in consistency of technical analysis is 4 out of 5, and Rallis is Somewhat Consistent in terms of financial performance.

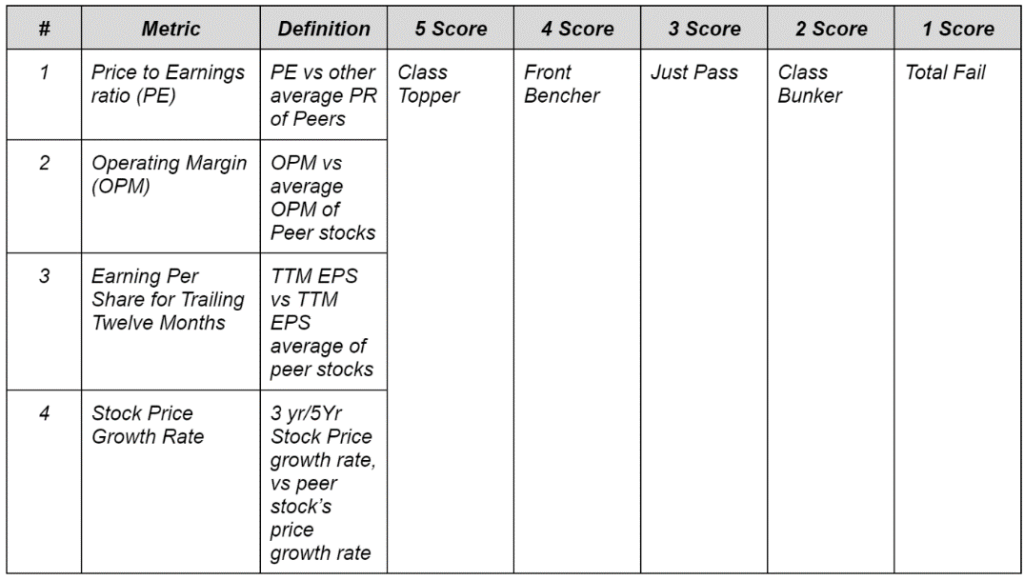

Peer Group Comparison: Class Bunker (2 / 5)

Rallis Peer Group Comparison: Rallis is compared with other small cap stocks in Agrochemicals space, such as Chambal Fertilizers, and Midcap stocks such as UPL, Bharat Rasayan, and India Pesticides. (a) PE; Rallis PE is higher than peers. Rallis PE as on Nov’21 is 30, whereas its small cap peer Chambal Fertilizer has PE of 10. MidCap peers also have lower PE of 20-27. (b) OPM: Rallis OPM is lowest among its peer stocks. Rallis OPM is at 11%, whereas all of its peers OPM is in the range of 20-30%. (c) EPS: Rallis EPS is the lowest among all its peers. Rallis TTM EPS is 10, whereas its peer stocks EPS varies from 12 to 370. (d) 3Y % Sales Growth: Rallis three year Sales Growth is the lowest among all peer stocks. Rallis’ 3Y % Sales Growth is 11%, whereas its peer stocks’ 3Y Sales Growth is in the range of 12% to 37%.

Owing to this comparison, Rallis is the worst performing stock when compared with its four other peer stocks. However, Rallis is just at par with the industry average metrics, hence I have given it a 2 out of 5 score.

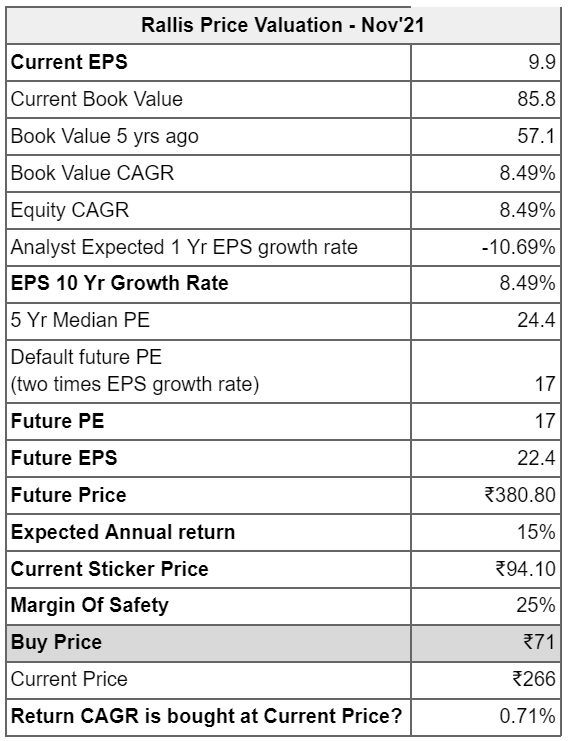

Valuation: Fairly Priced, Underperforming Stock

Fundamental Analysis – A below average company

Management (5/5)

Pedigree: (5/5)

Rallis Leadership is highly experienced, from tier 1 colleges of India.

CEO: Mr Sanjiv Lal is BTech from IIT Delhi, and Exec MBA from IMD Switzerland.

COO: Mr Nagarajan, is BTech from IIT Madras, and MBA from IIM Ahmedabad.

CFO: Subhra Gourisaria, is Chartered Accountant from The Institute of Chartered Accountants India (ICAI).

Experience: (5/5)

CEO: Mr Sanjiv Lal brings over 35 years of experience, with 21 years in HUL, and remaining 14 years in various Tata group companies

COO: Mr Nagarajan, brings over 30 years experience working in various Tata group companies.

CFO: Subhra Gourisaria, brings over 20 years of work experience, with 5 years in ONGC, and 14 years in HUL (Hindustan Unilever).

News (5/5)

Fraud related news: No Fraud in the news

No fraud related news by google search, and on stock analysis platforms such as tickertape, finology, moneycontrol is found for Rallis, or about their senior management.

Other news: ICICI securities has downgraded Price forecast for Rallis from INR 400 to INR 305 (link)

Rallis is seeking No Objection Certification to undertake research experiments on certain pest resistant crops (link). Even though this news is good, we do not know the percentage of revenue invested by Rallis in R&D, hence standalone this news does not impact our review of Rallis stock.

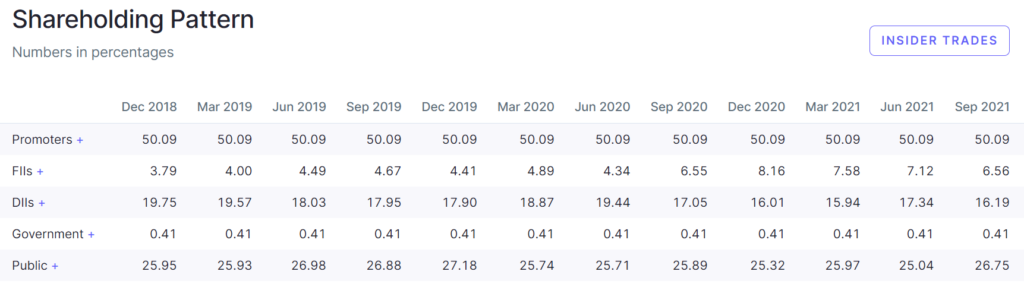

Holding: (3 / 5)

High Promoter holding, decreasing Foreign and Domestic Institutional Investors (FII and DII)

Regulatory Risk (2 /5)

Government interventions/policies can impact Rallis growth/profits. However likelihood of this happening is low.

Debt (5/5)

Negligible Debt – Debt to Equity of Rallis is 0.06, which is negligible. Interest Coverage ratio of Rallis is 45.44, which is comfortable.

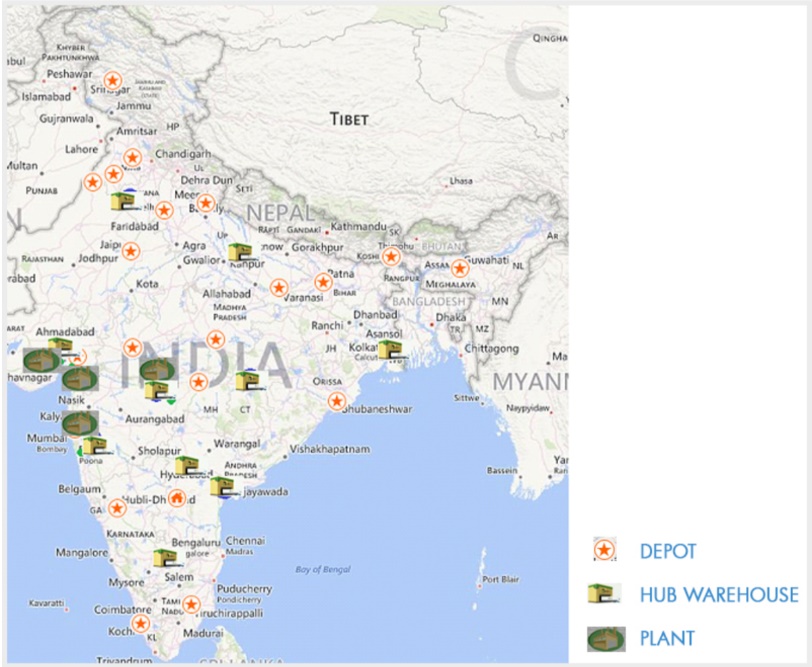

Distribution Control (5/5)

Rallis has good distribution across India. This will enable it to push new products into the market easily.

World Wide Web Analysis

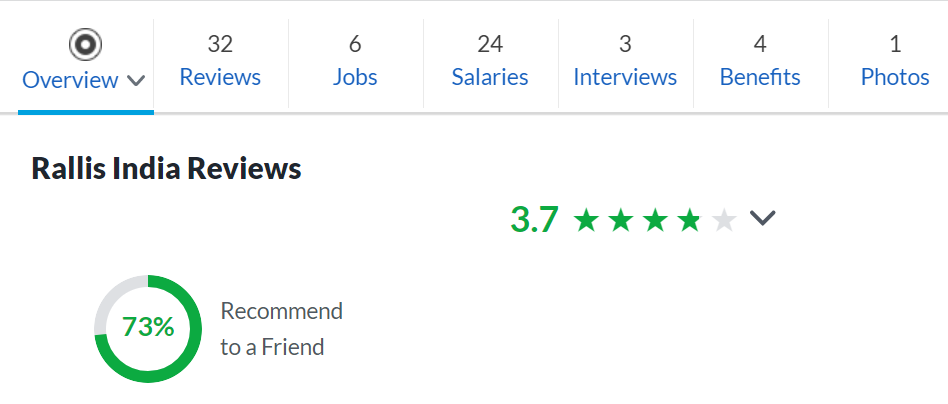

Company Rating (by employees):

3/7/5: Above average rates by employees on glassdoor.

4.3/5: Good company rating on ambitionbox.com

Digital Footprint

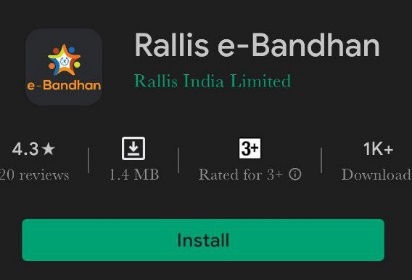

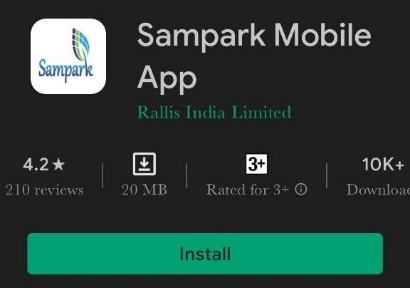

Rallis is making decent efforts in using digital technology to reach its customers, and serve them. It has launched two mobile applications to achieve this. All of its apps have 4+ Google Playstore ratings. However the number of downloads and ratings is less (<1k). Its two prominent apps are:

Sampark App: A mobile app ensuring better engagement with farmers, better visibility on reach mechanisms and insights gathering. The app assists in getting data with respect to demand creation activities and customer databases.

Krishi Samadhan App: A mobile app that provides relevant information regarding agri-solutions. It is a one-stop solution for farmers’ needs with features like customized package of practice, weather information, mandi information, crop solutions, complaint/query resolution, and personalized advisory through farm visits.

Third Party Views on Rallis

Overall, reviews of Rallis by third party sites and rating agencies in India is positive. This is driven by stable financials, reliable parent company (Tata Chemicals), and stable performance in the past as well as future prospects. Having said that, these sites also forecast a less than Nifty 50 Index growth of this stock.

CRISIL Rating (reaffirmed AA+ Oct’21 – Link)

Strong growth in 2021 (8%) driven by domestic market (63% of overall revenue), as well as stable international revenue.

Rallis financial profile is stable, with negligible debt, and healthy surplus liquidity.

Rallis strong focus on exports, branding, and farmer relationships.

Ratings take parent Tata Chemicals’ rating and size into account, hence may reflect standalone rating of Rallis as a company.

Tickertape

Only 44% analysts have suggested to buy this stock on tickertape, which is a low number. The stock price upside in the next year is estimated at 12.44%, which is less than average Nifty 50 index growth in the past 20 years

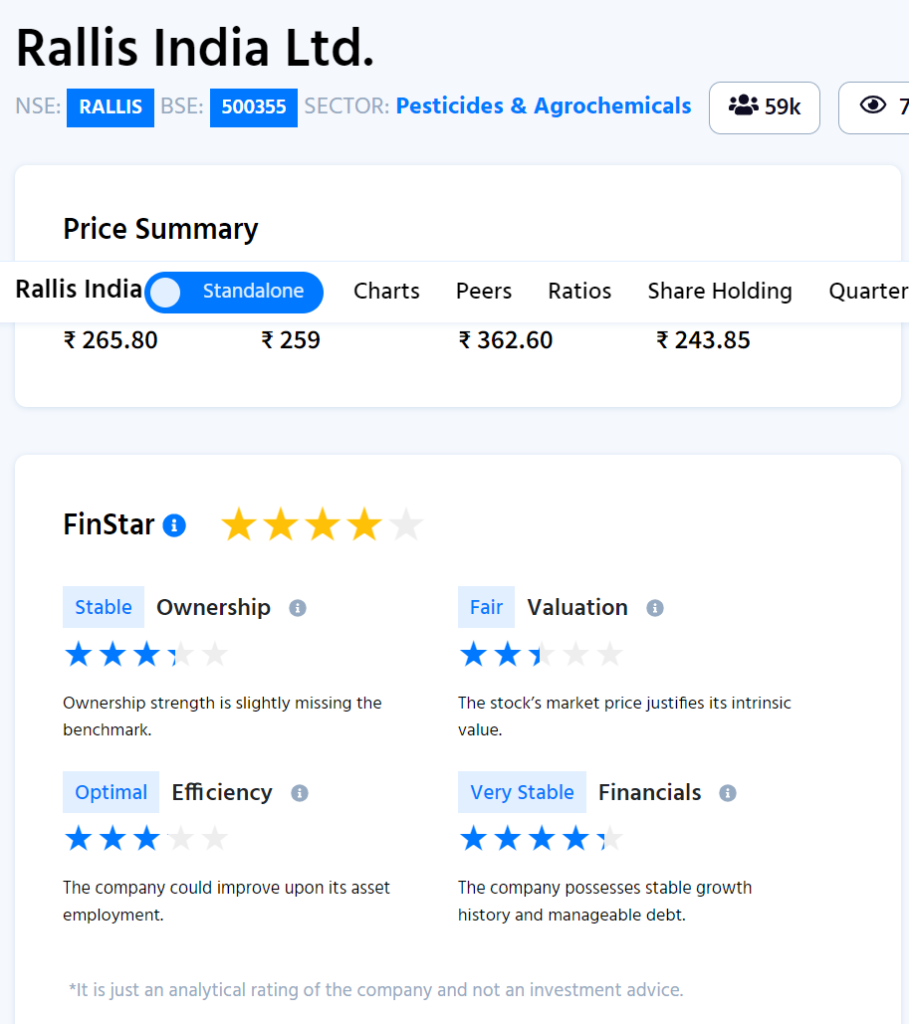

Finology

Finology has give a four out of five star rating to this stock, which is good. This is derived from stable ownership based on promoter holding, fair valuation based on PE, stable financials basis historical growth and debt, and good efficiency rating driven by return on capital employed metric.

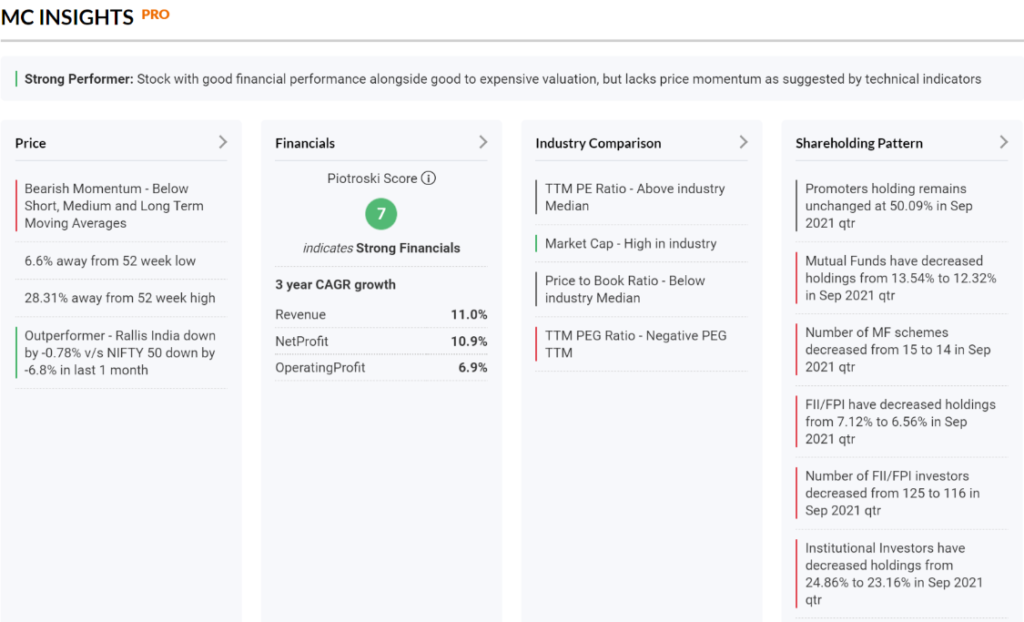

Moneycontrol

Moneycontrol rates Rallis as a company with stable financials, fair valuation, however poor price momentum.

Star Investor

Rakesh Jujhujwala, holds 9.81% of stocks. However, his holding in the company is down 0.50% from 10.31% in Sep 2020

Two Things I liked about Rallis

Like 1: Focus on Brand Building

In Oct’21 conference call, CEO Mr Sanjiv Lal mentioned the company’s continuous focus on building a new brand architecture, which will simplify brand understanding, improving brand recall. New products are being rolled out in the new brand architecture. One Rallis initiative focuses on using the same brand across seeds and crop care products, allowing it to present the same face to the trade and to the farmers.

Like 2: Capital Investment and Parent Group advantage

Rallis announced capital expenditure of INR 250 crore for the financial year 2022. Their expansion plans for setting up a formulation plant in Dahej (expected completion by H1 2022), and debottleneck units at Ankleshwar is proceeding as expected. Rallis has advantage of having a large parent group – Tata Chemicals, enabling long strategic advantage, and cash flow support in case there be need.

My Top Three Concerns with the company

Concern 1: Weak Futuristic Mission

Even though Rallis mission statement is to help farmers through science, there is less mention of future strategy to include modern technology to benefit farmers. Rallis is not planning to use artificial intelligence to help farmers predict weather (humidity, rainfall, sunlight conditions etc.), and plan seed planting, plant care, and watering/pesticide/manure spraying stages. Other players such as IBM, Wipro are planning experiments use AI to help farmers. Rallis, to me, looks like focused on production and distribution of seeds/fertilizers/pesticides, and not gear towards using modern tech like AI, drone based pesticide spraying etc., hence it is a less exciting company to me from future growth perspective. The same is reflected in R&D spend of the company, which is a meagre 1.5% of revenue. This, for a R&D focused company gearing for rapid future growth should be in the range of 5-6% of revenue. In comparison, other better performing companies in crop care/seed segments have higher R&D spend such as PI Industries (4% of revenue for R&D spend), and UPL (2.3% of revenue for R&D spends). This makes the current risks such as erratic monsoons, impact their sales easily.

Concern 2: Lack of industry expertise in top management

Even though top management are tenured people in TATA group, and have good experience in leading companies in India, they seem to lack expertise in crop care and seed sector. There are some signals to indicate this. First, in Oct’21 conference call, it was mentioned that Q2’21 seed business segment performance was poor owing to high demand for illegal herbicide tolerant cotton seeds. A good company leadership will focus on building solid feedback from ground operations, and act proactively, rather than reactively declaring the reason for a bad quarter. Secondly, since R&D is a long term project, having knowledge of risks involved such as cheaper substitutes, illegal products available, competition, feedback loop from real farmers etc. is important to have. Else the R&D investment may go to waste (sunk cost), and demoralize the R&D team for future new product development. In the Oct’21 concall, the management’s answers did not provide deep insights into the business. Example: on the lukewarm performance of millet seeds, the CEO Mr Sanjiv mentioned that the farmers did not pick up this crop. This is a high level answer, without insights which can uncover opportunities to rectify mistakes and stir future growth. The team at Rallis may want to explore using the 5 Why Root Cause Analysis framework.

Concern 3: Non convincing plan to address risks, and build moats

A great, forward looking company acts to minimize its risks, and build moats for a long term play. This does not seem to be the case for Rallis. Even though Rallis management accepts open risks to the company, there is no firm strategy in play to minimize these risks. Example: Inability to pass on the price increase from raw materials and supply chain to the end consumers. If farmers cannot pay more, why not ask for government subsidies, or enable a farmer lending program? Why not sell to distributor companies, or hold larger inventory for long shelf life products? Why not evaluate vertical integration, so that raw materials can be produced by your parent company – Tata Chemicals? Why not have strategic contracts with raw material suppliers which diversifies geographical risk, and also keeps the supply chain costs low? From the concall, it seems like the management is taking some steps, such as trying to procure raw materials indigenously (locally), however there is no certainty in the reply of the management of by when will these risks be addressed, and the answers to handle these risks are generic and into the future.

My Investment Decision

As on Nov’21, I would sell this stock if I still hold it. If I am a new investor, I will avoid investing in Rallis. The reason is that Rallis stock price has grown less than the Nifty 50 Index average for the past 5 years (5% Rallis Stock Price CAGR growth, vs 15% for Nifty 50). Rallis fares poorly in technical analysis when compared with other peers in the industry. Fundamental analysis of the company is below average. Experienced management with less sector expertise, weak future growth strategy, and having uncontrollable risks such as irregular monsoons, poor brand recognition by farmers etc. make this is a slow growing company, and hence a slow growing stock from price perspective.

When to Invest?

This is a cyclical stock, and investors can choose to invest in this stock during Mar-April, and exit the stock during Sep-Oct timeframe. Q1 and Q2 are the biggest sale quarters for Rallis, followed by drops in Q3 and Q4, hence you may want to invest at the end of Q4 (Mar-Apr), and sell off or exit at the end of Q2 (Sep/Oct).

Note that this cyclical nature may change in the future as international exports grow, and have a larger share in the Rallis’s revenue; or if Rallis launches more products to have good revenue growth round the year.