0. What is this post about?

Investing goals vary from person to person – from wealth preservation, to retirement planning etc. Investors in the equity market invest for wealth generation over time. Investors invest in equities via various means. Some of these are Mutual Funds (MF), Portfolio Management Service (PMS), and self-stock picking (Self Investing). Which of these ways gives the highest return on investment? Well, the answer is not straightforward. In this post, I will answer this question, based on my experience, and help you make a conscious choice between these three investment options.

Ready to pick an investment method which maximizes your returns? Let’s get started!

1. Types of Equity Investors

In order to find the right means of equity investing which maximizes returns, the prerequisite is to understand what type of equity investor you are. Equity investors are of various types. Many investors are salaried employees, who get a regular monthly paycheck. Some investors are business-owners.

Some investors are retired individuals, with a decent fortune to invest. Do note that retirees are not generally elderly people above 60 years of age. The retirement age is going down, and people are choosing to retire as early as 40 years of age in India, and globally.

If you are a salaried individual, a SIP (Systematic Investment Plan) format of investment is a good option. SIP enables you to invest small money, regularly (say monthly), in the equities via MF.

If you are a business owner, you may get large sums of money occasionally which you may want to put away for investment. A one time lump sum investment is not recommended. Hence for a lump sum investor, it is better to go via Portfolio Management Services, who manage large sums of money, deploying them at opportune time, in the right stocks to generate healthy returns.

A third type of investor is someone who is willing to learn and self- invest in the stock market.

To categorize the type of investor, I will divide investors into two types – Passive and Active investors. Passive Investors are either salaried employees, or business men, who want a professional to manage their money. Active Investors, on the other hand, actively invest their own money in the stock market. Active investors can be just about anyone – a salaried employee, a full time investor, a housewife, a retiree, a college student.

If you have INR 100/- to invest, then you are an investor.

Were you able to save your last three months’ pocket money? You can start investing now.

You are not sure whether equity investment is right for you? Start investing, and you will learn along the way.

Now, we know that you are an investor, and what type, let us understand some characteristics of an investor which will help us decide which equity investment method is a good choice for you.

2. Investor Characteristics

This section will help you understand yourself as an investor. Once you know yourself better, you can take a call on the right way for equity investment.

2.1 Investment Goals

Every investor has investment goals. Lets understand this from some examples.

Example 1: College Education fund: parents start investment as soon as their kid is born, for his/her college education. Their investment horizon is 18-19 years, by the time their kid joins college.

Example 2: Buying a House: A couple starts investment the day they get married, with the aim to buy a house in 5 years. This couple’s investment horizon is 5 years.

Example 3: A salaried employee at age 35, decides to invest for a peaceful retirement at the age of 50. This salaried person’s investment horizon is 15 years.

Example 4: A newly retired person at the age of 62, has a lump sum amount of INR 1 Crore. This retiree has no end goal, but to grow his fortune, and then to pass on his wealth to his kids once he passes away. This retiree has an indefinite investment horizon.

As you would see, investment goals decide the number of years you want to be invested in the equity market. I would recommend all equity investors to remain invested for at least 3 years. If you are invested for less than three years, you may go through a bear cycle and lose capital. If you exit your equity investment too soon, within a year, you will be paying a higher tax (15%), vs if you hold investment for more than one year, for which the tax rate is lower (10%). To truly experience the joys of compounding, you should stay invested longer in the equity market.

2.2 Risk Taking Ability

Every person has varying ability to take on risk. A person at the start of his/her career can take more risk. It matters not if this young person’s investment goes to zero, as he/she has a long career ahead to earn more money, and invest more. On the other hand, a retiree is risk averse. His main aim is to preserve the capital he has amassed over his past career. This retiree is ok with a lower return which beats inflation. Your risk taking ability determines the type of equity investments you should undertake.

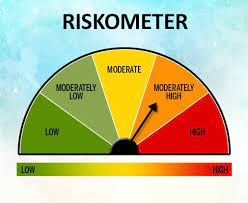

To standardize the riskiness of an equity scheme, all MF and PMS display a risk-o-meter on their funds and website. A typical risk-o-meter looks something like below. This meter gives an indication of the risk involved in investing in the said PMS or MF. Typically, if the equity scheme invests in large cap stocks (large, stable companies), the risk-o-meter is low to moderate. Equity schemes investing in small or microcaps have a very high risk-o-meter.

2.3 Time Investment

“You need 10,000 hours to master a new skill”. Investing is a skill. The more time you spend in the stock market, the more you learn. Even veteran investors like Warren Buffet and Vijay Kedia, after an investment career spanning multiple decades, say that they are still learning new things from the stock market. The amount of time you have to manage your equity investments, determine the type of equity investment option you should go for.

If you have a hectic full time job, which leaves you with little to no time even during the weekends, then your available time for managing your investments is zero. On the other hand, if you work an 8hour shift, and are willing to carve out 2 hours daily to track stock market, research stocks etc., then you can spend north of 14 hours per week on managing your investment. If you are a full time investor, you have ample time to learn, invest, and track. Rakesh Jhunjhunwala is a good role model for any full time, self-investors, who made a fortune from stock investments.

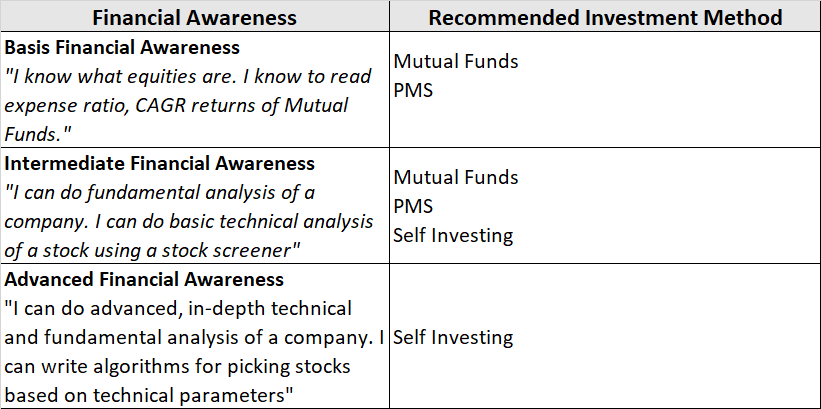

2.4 Financial Awareness

One needs some financial awareness to invest in equities. The decision to invest is an outcome of financial awareness. This awareness can come from experience, mentorship, educational degree, or self-education via books and online courses.

Basic financial awareness refers to knowing what equities are, what mutual funds and related categories are, what are large caps, small caps etc. Basic financial awareness based investing requires investors to spend zero to minimal amount of time towards managing their investments.

Intermediate financial awareness indicates ability to do fundamental analysis of a stock, and do basic technical analysis. Fundamental analysis includes reading a company’s annual shareholder presentation, understanding industry sectors etc. Basic technical analysis requires ability to comprehend top 4-5 technical indicators such as ROE (return on equity), OPM (Operating Margin), NIM (Net Interest Margin), Revenue CAGR (Cumulative Aggregate Growth Rate) etc. Intermediate financial awareness requires investors to spend 2-3 hours per week to keep track of macro economic trends, study company performance, and rebalance stock portfolios.

Advanced financial awareness indicates ability to do deep research into technical and fundamentals of a company. This indicates the ability to study and analyze financial statements of a company. An advanced investor can run Valuation models such as DCF (discounted cash flows), and even create own algorithms for stock picking and back testing them to analyze returns. Getting to an advanced level requires investors to spend a significant amount of time learning the art and science behind investing.

The level of financial awareness requires regular time investment to maintain that level. An advanced skilled investor can become intermediate if he stops spending time tracking markets, and researching companies. Basic skilled investors is the only category where you can maintain this level zero state with zero time investment – hence rightly called level zero!

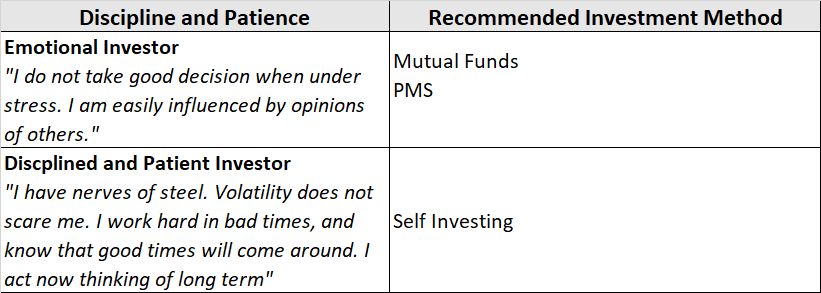

2.5 Discipline and Patience

Making money in the stock market requires both discipline, and patience. Discipline is needed to make investment decisions of buy and sell without emotions. Patience is needed to allow compounding to work and generate wealth. Stock market volatility is not for the impatient investors who buy in hope, and sell in panic.

You should introspect to determine if you are a disciplined investor. Do you have the ability to be patient along your investment journey? If daily price fluctuations increase your stress levels, it is better to leave your money with a professional investment manager. However, if you can do research to pick stocks, survive the volatility of the stock market, and course correct your portfolio, you are sure to reap higher benefits in the long run.

Having known the five characteristics of you – the investor, we will understand the three ways of equity investment in the next three sections, starting with Mutual Funds (MF).

3. Are Mutual Funds for you?

3.1 What are Mutual Funds?

Mutual Funds are funds managed by professional fund managers. These managers have undergone financial education degrees, and have decent experience (5+ years) working in equity or debt investment funds. Mutual funds can invest in equities, debts funds, or foreign equity funds. Without going into details of different mutual fund types (maybe a topic for another blog), let us understand if mutual funds are the right fit for you.

A mutual fund takes your money, and invests it in the equity market. In return for their services, mutual fund houses charge an expense fee, which typically varies from 0.1% to 2% annually. An equity mutual fund gives returns in the range of 12-15% annually to its investors. If you invest in high risk, high return mutual funds such as Small Cap funds, then your return may be higher in the range of 15-18%. If you are keen on knowing the mutual fund investment approach, I have written a separate post on the same – Mutual Fund Way of Investing.

3.2 Pros of Mutual Fund Investing

3.2.1 Your Money is Safe: Many investors want to invest safely, and are happy with average to above average investment returns. Investing in mutual funds is safe. You will not lose your capital. Even when the market undergoes a downturn, mutual fund managers will manage your money well, and generate positive returns over time.

Example: During market down cycle, Mutual Fund (MF) manager moves part of your invested money to cash, and waits for upcycle to invest again. MF managers can also choose to rejig the portfolio, and invest in defensive stocks during market downcycles. Defensive stocks fall less than growth stocks, and rise less than growth stocks during an upcycle. You can be rest assured that your money is in safe hands.

3.2.2 Ideal for Busy People

If you are busy, and cannot find time to research stocks on your own – mutual funds are for you. You need absolutely no research to invest in mutual funds. Do you trust a mutual fund brand, such as HDFC, ICICI, Tata, Canara, Kotak etc.? If yes, then invest in any of these reputed MF brands. You can not go wrong with any of the reputed MF brands. Your overall returns may vary slightly if invested in one MF brand vs another. But the difference is very small for you to worry too much.

Having said that, it is better if you can research a little on which MF scheme is best suited for you. This way, you know what the expected returns are, and what is the investment horizon you should invest for. Do note that you should never put your emergency funds in equity MFs, as equity MFs are meant for long term investments.

3.2.3 Inflation Beating Returns

MF will beat the inflation, and give you at least 10-12% annual returns. In India, historical inflation is at 5%. Keeping your money in a savings account gives you only 3-4% interest. Investing in Fixed Deposits gives you only 5-6% returns. Post tax, these returns will degrow your money when adjusted for inflation.

Assuming average inflation in India at 6%, and 30% income tax slab, you need at least 8.6% annual returns to just beat inflation. An 8.6% and above returns are only possible via equity investments, and in some select cases via debt funds.

3.3 Cons of Mutual Fund Investing

3.3.1 You will not make the highest returns from equity investment

You will be making average returns of 12-15% annual returns. But, you should know that you can make even higher returns from equity investments. Yes, you can make as high as 25-30% annual returns from the stock market. Portfolio Management Service (PMS), and Self Investing are these methods, where you can make more returns. Let me explain this point a bit.

Let us say, you invest INR 10K in a MF scheme. The MF scheme will immediately buy the portfolio of stocks in the scheme, on the day you invested. Let us say on the day you invested, the stock market was overpriced. Which means that as the market corrects in future, your investment will decrease. However, if you would have invested in a PMS, or self-investing, you will wait for the valuation to become reasonable before you invest. This way of investing in only fairly valued stocks, or undervalued stocks, generates higher returns.

3.3.2 Cost of Mutual Funds

As mentioned in section 3.1, MF houses charge an expense ratio, in return for offering their services. Even though this expense ratio looks low (0.1% to 2%), this percentage over a long term, say 10 years, does lead to a sizable chunk of your returns.

Example: If you make a one time investment of INR 1 Lac (INR 1,00,000), in a MF with an expense ratio of 0.5%, assuming 15% annual returns (minus 0.5% expense ratio), your investment value after 20 years will be INR 1.6 Lac. However, if you invested on your own, making the same annual return of 15% annually, without any expense ratio, you would have ended after 20 years with INR 1.74 Lac. This is 9% higher than a similar MF scheme.

3.3.3 Not Ideal for the Ultra Rich

As such, Mutual Funds do not have an upper limit of investment amount. However, some Mutual Funds schemes may limit investment amounts. Example: Mirae Bluechip Equity fund limited SIP amount to INR 2500 starting 2021. Some mutual fund schemes can close further investments as well, owing to regulatory changes, or just because the fund has become big enough to consistently deliver good returns.

3.4 Mutual Fund Summary

Mutual Funds are a good option if you are a salaried person, with limited capital to invest, and have no time to research stocks on your own. You are not an aggressive investor, and are ok with average equity returns in the range of 12-15% annually. If this is you, then swipe right to Mutual Funds, and start investing :-).

Mutual funds work better for persons who are disciplined and patient investors. MF also has a great way of instilling discipline – SIP or Systematic Investment Plan. Setting up a SIP automatically debits a defined amount from your bank account every month, at a selected date. This removes the personal motivation needed to invest every month.

One should note that there is a fourth investment option known as smallcase (https://www.smallcase.com/), or vests (vested.co.in). These are closer to MFs, as they work in a similar fashion. You can set up SIP in these smallcases. When you invest in a smallcase, all your money is invested instantly. These small cases do have a maximum amount of investment allowed. The advantage of small cases is that the process feels more real, as you know all stocks you are buying and selling, and gives you the option to customize the number of stocks being bought or sold. However, customization is not recommended, as this will deviate your smallcase from what the small case manager has designed.

Mutual funds are not the best option if you want higher returns (north of 15%/year), and are willing to allocate time to learn, research, and track investment portfolios. I will talk about self-investment style in section 5 shortly.

Are you ultra-rich, with a large lump sum amount to invest? Then PMS might be a right fit for you. Lets know more on PMS in the coming section.

4. Is Portfolio Management Service right for you?

4.1 What is a PMS?

PMS, or Portfolio Management Service, is a professionally managed investment service. Investing in PMS requires high capital, usually more than INR 50 Lacs or more . PMS customizes investment strategy as per investor’s needs. PMS manager can invest across multiple asset classes, such as equity, debt, real estate.

PMS charges a tad higher fees than mutual funds. The fee structure varies from one to another PMS, but is typically more than 1% of total investment. The PMS fees can either be a flat fee, or a combination of flat fee and profit sharing fee. Say, 1% flat fee per year, and 20% profit sharing if annual profits are more than 15%.Some well known PMS providers in India are Marcellus (https://marcellus.in/), Capital Mind (https://get.capitalmind.in/wealth), ICICI (https://www.icicidirect.com/services/portfolio-management-services). PMS are offered either by banks, or by SEBI registered investment advisors.

4.2 Pros of PMS

Pros of PMS are very similar to that of the Mutual Funds, mentioned in section 3.2. These are namely: (a) Safety of Money (b) Ideal for busy people. (c) Inflation beating returns.

When compared with Mutual Funds, PMS can generate higher returns. However, this point is often contested (read Economic Times article on this topic here). Given that the cost of using PMS is higher than MF, the net returns of PMS and MF may be comparable. However, on an average, PMS does give higher returns than MF.

For an investor to generate higher returns via MF, one will have to do some research, and invest in high risk, high return MFs, such as small cap MFs, thematic MFs such as investing in IT or technology themed MFs. For an average investor who invests in safe MFs, such as index funds, or large cap MFs, will not be able to beat returns from PMS.

4.3 Cons of PMS

4.3.1 Cost of PMS

PMS costs more than mutual funds. Their fees are usually >1% of total investment amount. This is still ok, as you can earn in the range of 15-20% annually from PMS. Unless you have time, and financial awareness to select stocks on your own, you are better off using a PMS to generate index beating returns.

4.3.2 Minimum Investment Barrier

PMS requires a minimum amount of investment, which is usually very high for normal retail investors. PMS typically onboards investors with more than INR 50 Lacs of capital. This high capital acts as an entry barrier for many retail investors, who are unable to use PMS. To tackle this, many PMS offer smaller investment options such as MF, smallcases etc. However, if you want higher returns, and customized investment strategy across multiple asset classes, then PMS is the way to go.

4.4 Portfolio Management Service Summary

PMS, or Portfolio Management Service, is a good fit for those investors who have large capital to invest (north of INR 50 Lacs). PMS is costlier than MFs, but also generates higher returns. One can expect to get returns between 15-20% annually from PMS.

PMS funds are adopting technology well, and now provide a transparent, easy to use online dashboard for investors to track their investments. With the increase in millionaires in India, the future of PMS looks bright, as more people with large capital choose a customized investment vehicle offered by PMS.

Minimum Investment Capital barrier keeps the majority of retail investors away from PMS. However, with the right level of financial awareness, an investor can pick a set of high risk and high reward MFs to generate returns equivalent to PMS, and at lower costs.

Are you an investor who likes the thrill of self-picking stocks? Do you want the highest returns from equity investments, more than 20% per year, maybe even 30% or more? If yes, then read on to the next section of the Self Investment method.

5. Is Self Investing right for you?

5.1 What is Self Investing?

Self Investment means picking stocks on your own, making your own investment portfolio, managing your own portfolio. You do not hire a professional investment manager. You are the manager. You research and invest in stocks you believe will give returns over time. You rebalance your portfolio regularly, to sell poorly performing stocks with little room for future growth, and investing more in good stocks.

With self-investment, the investment returns may vary. You can get very high returns, beating returns from MF or PMS. On the other hand, you can get very low returns as well, if your investment decisions are not well researched.

5.2 Pros of Self Investment

5.2.1 Highest Returns Possible

You can achieve the highest returns possible from stock market investments. MF and PMS main aim is to protect capital, and grow it wisely over time. However, as a self investor, you can take higher risks, and get higher returns. You can choose to invest some, or all of your money in risky bets (say small caps), and reap the benefits if some of these companies become multi-baggers (multiply your wealth).

Do note that it requires decent time investment (north of 4 hours per week), to research and track companies, macro environment, to actually make good returns.

5.2.2. No Costs

Self investment has zero costs involved when compared with MF or PMS. You do not pay any expense ratio. You invest based on your research, and are responsible for the returns you generate.

Do note that for self-investing, the costs are not actually zero, as you will end up paying brokerage fees on the platform you use to create DMAT account, and perform investing trades. However these are minimal and negligible. Example: On Kite Zerodha, annual account maintenance charge is INR 300/-, buying shares is free, selling shares has a minimal fee of INR 18.

You will also indirectly pay the cost of your time, as you will need to invest 4+ hours every week to research stocks, track performance of the companies you have invested in.

5.2.3 The Thrill of Investing in Stocks

Many investors do self-investing in stocks for the thrill of it. Investing in individual stocks, and seeing the returns turn green, and greener week on week is a satisfying feeling. As compared to MFs, where there is little transparency on the underlying invested stocks, or how these stocks are contributing to your returns, self-investing gives you a real-time view of profits or loss from the companies you have invested in.

5.3 Cons of Self Investment

5.3.1 Possibility of Erosion of Capital

This is the opposite of pro mentioned in 5.2.1. If you make poor investments, or invest all your money in just 1-2 stocks which go bust, you can actually erode your capital. This means, you will generate negative returns, and lose the investment amount. This is one area where MF and PMS have an advantage. MFs and PMSs will protect your capital, giving at least index average returns.

A good way to tackle this con is to start your investment journey using a combination of MF and Self Investing. You can bifurcate 90% in MF, and 10% in self invested stocks. As you gain more experience, you can divert more capital in self-investing. Once you start generating higher returns via self-investing over MF, consistently for over an year, then you can consider dropping out of MFs and only do self-investing.

5.3.2 Requires Discipline and Patience

Self-investing is hard. It really is. You may get lucky, and think of moving to self-investing entirely. And over time see your returns shrink. Why do you ask? Because investing requires discipline and patience. One needs to remove emotions from investing. Selling at market lows, and buying at highs is a bane, and normal investor behavior. Sound investing requires a kind of contrarian mindset, which thinks independently, and often acts opposite of the market mood.

Do not get me wrong. Picking good stocks is not hard, but simple, if researched properly. However, maintaining an objective mind, not panicking, not getting swayed away by euphoria are equally important. As an investor, you should test your investing discipline over a couple of years, before plunging 100% into self investing.

5.4 Self Investing Summary

If you are financially aware, can devote sufficient time to research and track company performance, then pick the self-investing route. Self investing, if done right, can generate the highest returns from stock investment. You can actually double your money every three to four years.

However, you should be aware that in self-investing, you are the captain of your ship. Your quality of research, and investment decisions decide the path your investments take – either to the land of multiplied wealth, or to the barren island of piling losses.

6. Parting Thoughts

We understood key characteristics of an investor in section 2. Then we reviewed the three most common ways of investing in the stock market in sections 3, 4, 5. In this last section, I will tie up characteristics of an investor with the recommended way of investing.

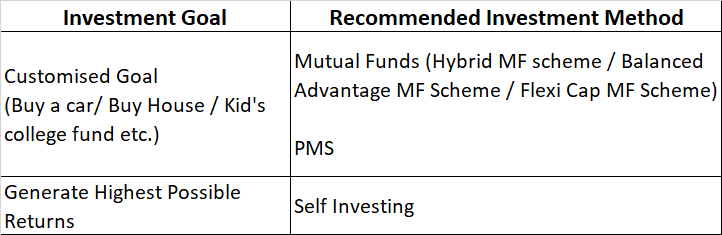

6.1 Investment Goal based investing method

MFs and PMSs are the better options if you have a specific investment goal in mind. These professionally managed services can manage risk, and invest across multiple asset classes to help you achieve your investment goal.

If your investment goal is to make the highest returns possible, with a long investment horizon, then go for self-investing.

6.2 Risk Taking Ability based investing method

If you are a low or medium risk taker, go with MFs or PMSs. These funds will protect your capital, and help it grow over time. They may or may not be able to beat the index (Nifty 50 or BSE 100). However, MF or PMSs will not erode your capital, and will definitely give you higher than Fixed Deposit returns.

However, if you are a risk taker, and are financially aware, go for self-investing.

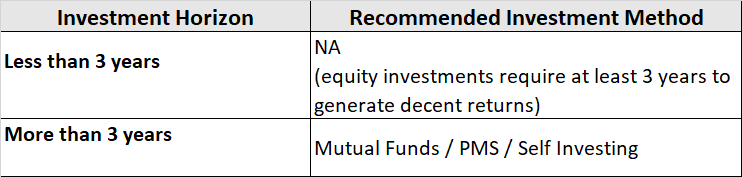

6.3 Time based investing method

If your investment horizon is less than 3 years, then I would not recommend investing in equities. Equities need at least 3 years to generate decent returns. For less than 3 years, consider alternate investment options such as short term debt. Do note that if you are lucky, and invest in a bull cycle, you can generate good returns in the short term as well (< 3 years). However, to enjoy the compounding effect from equities, an investment horizon of more than 3 years is recommended.

If you are busy with your job/business, and cannot spend time on stock research, then go for mutual funds or PMS. However, if you can spend north of 4 hours/week to research stocks, read news on macro economic trends, then you can choose to go down the self investing path.

6.4 Financial Awareness based investing method

Based on your financial awareness, you can choose MFs or Self Investing. If you have basic financial awareness, and still want to do self-investing to generate higher returns, you should find time to learn about investing, and then pick up stocks to self invest into.

6.5 Discipline and Patience based investment method

Emotions play a large part in successful investing. Confidence over hope, patience over panic, and consistency over luck is what matters.

I hope you are now better informed on choosing an equity investment method that suits you. Investing is a personal decision, and should be driven by your priorities and goals.

Which investment method do you prefer, and why? Do comment below.

Happy Investing!