What is the fuss?

HCL Technologies (HCLTECH), one of the top largecap IT companies, announced its Q4 FY 23 results on 20th Apr, 2023. Finally, this largecap is showing signs of slowdown, with a downward revenue growth guidance in FY 2024 (Apr’23 to Mar’24). In this post, I cover the main takeaways from Q4 FY 23 results, and share my views on what to do with this stock in FY 24.

HCL Tech — Company Overview

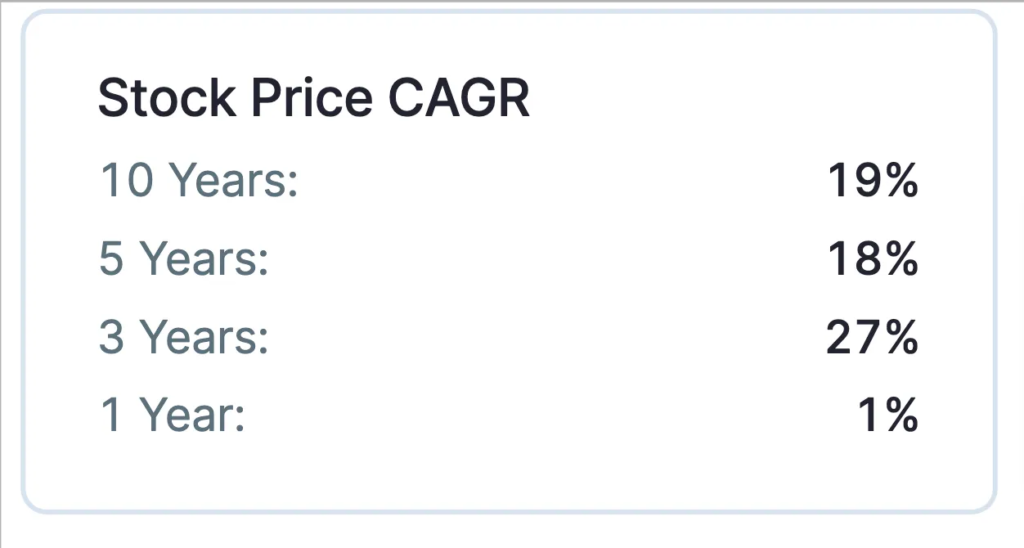

Wealth Generation for Investors: HCL Tech is a slow, consistent compounder in the IT sector. It has compounded investors wealth at an CAGR of 19%, over the past 10 years. This means doubling your money every 4 years. Not bad, not bad at all.

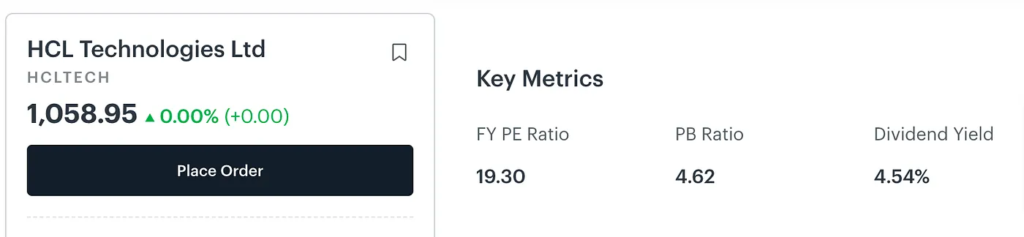

On top of this, the company’s doles out handsome dividends, which is north of 4% of its stock price. This makes it the highest dividend yield stock of the Indian IT sector.

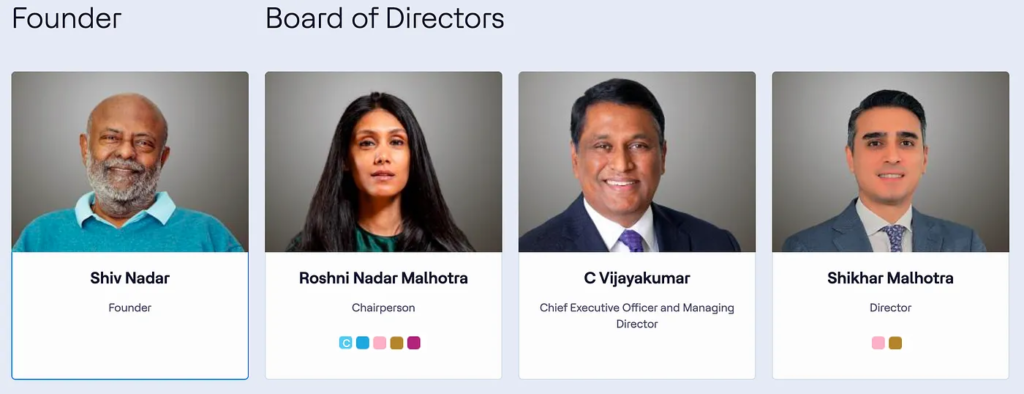

Experienced Management: HCL Tech was founded by Mr Shiv Nadar, and is now led by his daughter Roshni Nadar Malhotra, and his son-in-law Shikhar Malhotra. The current CEO of the company is Mr C Vijaykumar, who has been with the company for 30 years, almost since its inception!

Most of the senior management of the company, its CFO Mr Prateek, and Chief Delivery Officer Mr Apparao are also old timers in the company.

Experienced management, and with promoters holding more than 60% of the company gives confidence in the commitment and experienced leadership of the company.

Company’s Business Lines keeping up with time: HCL Tech has evolved from being just an IT service provider, to successfully entering new and emerging business lines — namely Engineering R&D, and Software as a Service. Now, the company has three main business verticals — The traditional IT & Business Services, the new HCL Software, and the emerging Engineering R&D services.

Q4 FY 23 Highlights

Positive highlights

- HCL Software business vertical reached annual 1 billion dollar turnover for the first time

- Company continues to have healthy free cash flow of USD 2 billion. This will help the company weather any recessionary period, and also acquire companies available at a discount or in distress..

- Attrition has normalised, reducing from 22% in Q4 FY 22 to 19.5% in Q4 FY 23.

Now, onto some not so good news.

Negative highlights

Most of the negative highlights revolve around FY 24 guidance. As per company’s comments, FY 24 will be a year of consolidation. This means the coming year will be boring at best. Less to no positive surprises. Flattish revenue growth.

- Revenue growth guidance of 6–8% in FY 24, 66% less from 18% revenue growth seen in FY 23

- Flat margin guidance — to remain at 18–19%. This is same as what the company achieved in FY 23.

- Slowing order book growth. Deal closure lead time is increasing. These are all signals of a soft recession in the west, resulting in companies turning cautious.

What am I doing with HCL TECH stock in FY 24?

I will continue to hold the stock throughout FY 24. This aligns with my long term investment strategy. I will look for opportunities to add the stock on declines. As of the date of writing this post in May’23, the stock is trading at 5% premium to its historical median PE of 18. Hence, I will wait for corrections more than 5% to consider buying HCL Tech.

My rationale for holding the stock, and accumulating more are:

Reason 1: Consistent compounder

HCL TECH is a consistent compounder. It may not give high alpha, but its beta is low. This gives predictability of investment returns, which I like. (Alpha means higher returns versus overall stock market index. High alpha is desirable. Beta means volatility vs overall stock market. Lower volatility is desirable).

Reason 2: Experienced and Committed Management

As I covered earlier in the post, HCL Tech is moving from first generation to second generation of promoters. In this transition, the executive leadership of the company is with employees who have been in the company for 10 + years. Experience, and commitment of company leadership is evident from high promoter holdings, and no news of leadership exits or ousting of management.

Reason 3: Buy the Downturn, enjoy the upturn

Multiple uncertainties in global economies, and continued war between Russia and Ukraine will lead to volatile stock market in FY 24. This is reflected in the bearish growth guidance from HCL Tech leadership for FY 24. This is a good time to accumulate fundamentally strong stocks. The growth story of IT sector, and HCL Tech remains intact. I am expecting IT growth to pick up FY 25 onwards. Hence, I will buy in FY 24, to reap rewards during the next upturn in IT sector in FY 2025 and beyond.

Reason 4: High Dividends

HCL Tech gives 4–5% dividends. This will come irrespective of stock price movement. The company has healthy free cash flow, which it distributes to its investors regularly. This is not an investment criteria for me, but keeps me happy during periods of consolidation or downturn.

Parting Thoughts

For existing investors, unless you are in dire need of money, you can hold on to the HCL Tech shares. This consistent compounder will give good returns in the next IT sector up-cycle.

For new investors, FY 24 is a good time to start accumulating HCL Tech stock.

HCL Tech may not give more than 20% annual returns, as compared with faster growing technology companies. However, it can very well become part of your core portfolio, which provide stability to your investments.

Key risks to watch out for are: (a) Deep and long recession in the US and EU (b) Increasing exposure to banks and companies who might default (c ) Growth of new business verticals. This is key to be relevant in the rapidly changing technology industry. (d) Key Person risk — no upheaval or ousting of top management.

Hope this helped.

Happy investing!

Disclaimer: I am not a SEBI registered advisor. Please do your own research before investing.

Do consider subscribing to my weekly email newsletter here.