How to make INR 12Lac passive income annually

Why INR 12 Lacs as Passive Income?

Many of us dream to be financially independent. Some of us methodically plan towards it. And a smaller percentage of us achieve it – Financial Freedom. The state where you no longer need to work for a boss. No longer, you need to live a life according to the vision and mood of someone else. You can, in reality, become the master of your time, and captain of your life story. You are able to generate enough passive income to sustain your lifestyle. Passive income is money generated from investments. This means, you do NOT have to work to make this income. You eat, sleep, repeat, and this income gets deposited to your bank account regularly . Isn’t this fantastic?

Well, all that is good to hear, but why INR 12 Lacs/year? This number is, just a number. For many individuals, INR 1 Lac per month is more than sufficient to fulfill your basic lifestyle needs, along with popping in some travel plans 3-4 times a year. With this logic, if you make INR 12 Lacs per year as passive income, it will fulfill your basic lifestyle needs. You will be in no pressure to work for bread and butter. This will give you confidence in your current work. Or, this will give you support to ditch your current work, and find the job you truly want to be in. You can even take some tension free time off, recharge yourself, and figure out your passion and a plan to pursue it.

The ideas beyond getting to the point of financial independent are unending. This post is to give you a fair idea of how much money you need, in order to be able to generate INR 12 Lacs per year as passive income. Lets get started.

Methodology Used

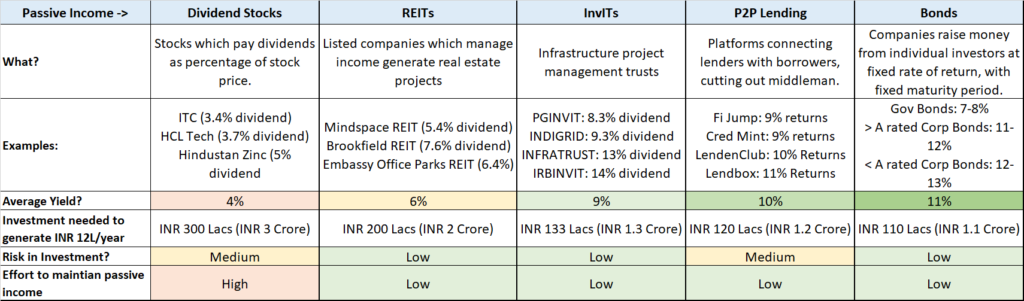

I will list and compare five passive income streams. These income streams will have following four evaluation parameters.

(a) Average Yield

This gives the percentage of passive income generate from invested amount. Example: If you invest INR 1,000, and your annual passive income from this investment is INR 100, then your Yield is (INR 100/ INR 1,000) = 10%. Higher yield is better, as you will generate higher percentage of income for the same invested amount. Yields shown in this post are taken as on Jan’ 2023.

(b) Investment to generate INR 12lac/year

This parameter tells you what is the total money needed to invest in only one passive income stream, to get INR 12 Lac/year. This is derived from metric a. If your yield is 10%, as in the example above, then to generate INR 12Lac/year you need (INR 12 Lac/10%) = INR 1.2 Crore per year. Lower the total investment amount, the faster it is for an investor to achieve the required passive income.

(c) Risks Involved

This parameter will provide risk of losing capital in the investments. I will categorize the final risk as High, Medium, and Low. This will be based on investment risk, and other associated risk such as default risk, macro economic risk etc.

(d) Effort Involved

This parameter tells how much effort is needed to track and adjust your investments generating passive income. I will provide three values for this parameter: High Effort means you will have to actively track and adjust your investments. Medium effort means you will have to spend less time, less frequently to track and adjust your investments. Low effort means you do not have to spend time or effort tracking and adjusting your investments.

Lets get started with the five passive income ways. My favorite way is towards the end :-).

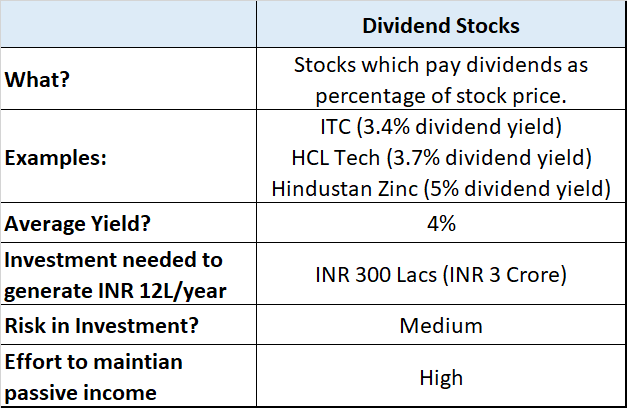

Passive Income 1: Dividend Yielding Stocks

What are Dividend Yielding Stocks?

Stocks which pay high dividend yield, are generally categorized as Dividend Yielding Stocks. Dividend is income distributed by the company behind the stock, to its shareholders. These dividends are distributed at different intervals, which vary from quarterly to annually.

Dividend Yield gives the dividend paid as percentage of stock price. Example: If you invested INR 1 Crore (INR 100 lacs) in a stock, and the stock gives 10% dividend yield, then you will get an annual dividend of INR 10 Lacs (slurp !). Higher the dividend yield, higher the passive income you can generate from same investment.

Typically, stocks pay less than 1% dividends. Many stocks, especially tech stocks, are known to pay zero dividend. The reason is that these companies prefer to reinvest their free cash into future growth of the company. One must choose companies which pay high dividend, and are growing well into the future. Without the latter criteria, there is risk of losing your invested capital.

Average Yield from Dividend Paying Stocks

High dividend stocks will pay dividends in the range of 3-4%. Some examples are below:

ITC (3.4% dividend yield)

HCL Tech (3.7% dividend yield)

SJVN (5% dividend yield)

Hindustan Zinc (5% dividend yield)

Note that I did not include PSU stocks such as SAIL. Many PSU stocks may erode your capital. That is, their stock price will not appreciate. PSU stocks work for social welfare, and pay high dividends to act as income source for the government. Government has majority stake in these PSU stocks, so it ends up getting majority of dividends distributed by these PSUs.

I did not include metal stocks such as Tata Steel. Metal stocks are highly cyclical. If you can time the cycle right, you can as well go for top metal stocks.

Investment to generate INR 12lac/year from Dividend Stocks

This is straightforward. Divide INR 12 Lac by 4% yield, which gives INR 3 Crore. You need to invest INR 3 crore to get INR 12 Lac per year as passive income from investing only in High Dividend Stocks.

Risk in Dividend Stock Investing

Yes, there is risk. One is stock market risk. Due to unfavorable macro economic situation, stock market may fall, including your dividend stocks. This will erode your invested capital. This may also impact dividends if the company decides to save up cash for its own survival, and weather the bad times.

Second risk is valuation risk. If you invest in dividend stocks at high valuation, your dividend yield will be low. This may not impact your dividend income, rather impact the stock investment returns.

Usually, high dividend stocks as mentioned above are large, stable companies. These companies are expected to pay out dividends for the next 5-10 years.

Hence, I will call overall risk in passive income from dividend stocks as MEDIUM. The reason is that there is some risk involved (market risk, valuation risk), but the risk not too high which can erode your invested capital.

Effort to maintain passive income from Dividend Stocks

Managing investments in dividend stock is high effort. Investor will have to screen stocks to create a portfolio of 5-10 stocks giving high dividend yield. One needs to do fundamental analysis of these companies to shortlist well managed companies, with good future growth strategy. You can choose to use GEMS framework to select stocks – Growing company, Efficient operations, good Management, available at Sale price. (read more on GEMS framework here under section 2).

One needs to review dividend stock portfolio every year, to evaluate rising or stable or decreasing yields. Depending on this exercise, you will rejig your portfolio to get required passive income.

As a dividend stock goes out of favor and enters slow sunset, one has to find new dividend company to invest in.

Investor also needs to invest at the right valuation. This will ensure gains on invested money as well.

Overall, maintaining passive income from dividend stocks is a HIGH EFFORT process.

Below table summarizes dividend stocks as source of passive income.

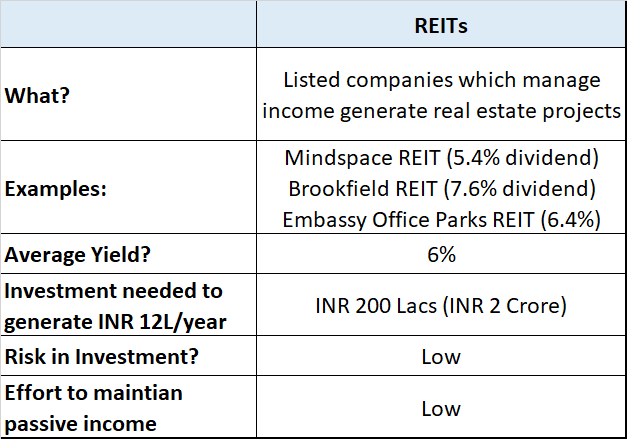

Passive Income 2: REITs

What are REITs?

REIT stands for Real Estate Investment Trust. REIT is a company that owns and operates income generating real estate projects. Typically, these real estate projects are commercial properties, which generate rental income. REITs are traded as stocks on the stock market. They distribute their real estate income to its share holders via dividend payouts. REITs reduce the entry threshold for retail investors like us, to enjoy passive income from large commercial properties. This is not a new concept, and is quite popular among passive income seekers in western countries such as the USA.

Average Yield from REITs

REITs give a yield in the range of 5-7%. Indian regulations require REITs to distribute at least 90% of the income generated by them to shareholders as dividends. Apart from dividend income, investors also benefit from appreciation in stock price of these REITs. Dividend yields from the three listed REITs in India are below.

Mindspace REIT (5.4% dividend)

Brookfield REIT (7.6% dividend)

Embassy Office Parks REIT (6.4%)

Investment to generate INR 12lac/year from REITs

Lets take average 6% as dividend yield from REITs. To generate INR 12 Lac/year passive income, you need to invest (INR 12 Lac)/6%, or INR 200 Lac or INR 2 Crore. This is less than INR 3 crore investment needed to generate same passive income from dividend stocks.

Risk in REITs

REITs have very low risk. REITs operate under SEBI regulations, which require them to have minimum 80% of their properties generate income. This means that REITs cannot have more than 20% properties which are under development. Secondly, REITs are required by regulations to distribute at least 90% of their income to share holders. Thirdly, REIT companies are usually large, reputed companies, with long history of good execution. Hence, overall risk in REITs is LOW.

There can be a minor risk, which is macro economic risk. Example, during COVID, many companies shut down or moved to remote working. This reduced the income of REIT companies. However, COVID like events are rare. Even when these events happen, the dip in passive income will be for a couple of years before resuming. As REIT companies are large, they have sufficient cash flow to survive such events and come out unscathed.

Effort to maintain passive income from REITs

Overall effort to maintain passive income from REITs is low. There are limited REITs listed in India, and all of these are reputed companies with long history of execution. REIT investments can be grown over time once their stock price is available at reasonable valuations. Apart from slowly building position in selected REITs, there is no major effort required in rebalancing your REIT portfolio. An investor should review their REITs investments at least annually. One should also evaluate any new REIT listing in the stock market from investment perspective.

Below table summarizes REITs as source of passive income.

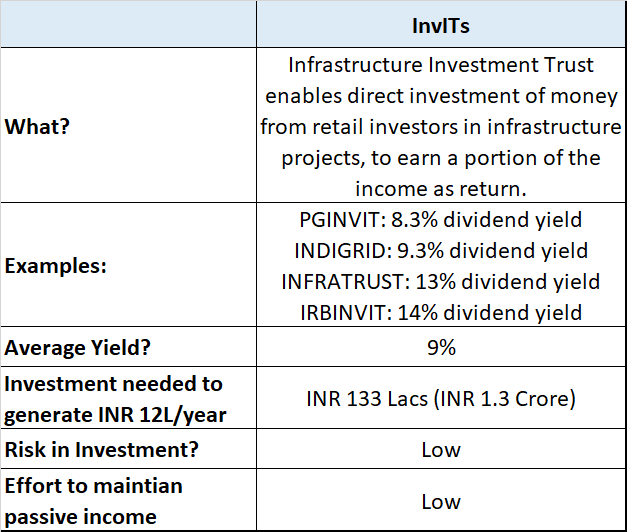

Passive Income 3: InvITs

What are InvITs?

InvIT stands for Infrastructure Investment Trust. An Infrastructure Investment Trust (InvITs) is investment scheme similar to a mutual fund. InvIT enables direct investment of money from retail investors in infrastructure projects, to earn a portion of the income as return.

The sponsor of InvIT invests into eligible infrastructure projects either directly or via special purpose vehicles (SPVs). InvITs can be set up by public or private companies. Example: Powergrid Corporation of India, a public sector company, has set up Powergrid Infratrusture Investment Trust (ticker signal: PGINVIT).

To know more about InvITs, you can read dedicated InvIT page on NSE website here.

Tip: InvITs are relatively new in the Indian stock market, and have not gained awareness. Therefore, many InvITs are trading at cheap valuations, and offer high dividend yields. It might be a good idea to accumulate InvITs during next couple of years 2023-2026, and benefit from higher dividends.

Average yield from InvITs

InvITs give an average yield of 9%. Income generated from infrastructure projects managed by InvITs are distributed as dividend income to its shareholders. Dividend yields of the some listed InvITs in India are below.

Powergrid Infra Investment Trust (PGINVIT): 8.3% dividend yield

India Grid Trust (INDIGRID): 9.3% dividend yield

India Infrastructure Trust (INFRATRUST): 13% dividend yield

IRB Invit Fund (IRBINVIT): 14% dividend yield

Some InvITs above give very high yield of 13-14%. These are abnormal because InvITs have less awareness. Secondly, some of these InvITs have less liquidity in the stock market, making it hard to buy and sell at ease. Therefore I have considered slightly lower average dividend yield of ~9% for InvITs.

Investment to generate INR 12Lac/year from InvITs

In order to generate INR 12Lac/year as passive income only from InvIT investments, one needs to invest (INR 12Lac)/(9%), or INR 133 Lacs. In other words, you need to invest INR 1.3 Crore to get yearly passive income of INR 12 Lacs. This investment amount requirement is lower than INR 3 Crore for dividend yield stocks, and INR 2 Crore for REITs.

Risk in InvITs

InvITs are regulated by SEBI guidelines. There is strong governance in allowing InvITs to list on the stock market. Similar to REITs, regulations required InvITs to distribute at least 90% of their income to share holders. InvITs need to have at least 80% of their assets in completed and revenue generating state. InvITs are usually sponsored by public sector companies or reputed large infra companies.

The underlying assets of InvITs include highways, power transmission etc. These assets have long life, and multi-decade licenses to collect revenue. Hence, there is very low risk in InvITs. One needs to be careful to enter InvITs at fair or cheap valuations. This will help investors to also make returns from stock price appreciation.

Effort to maintain passive income via InvITs

There are only five listed InvITs in the Indian stock market. Out of these, you can choose 2-3 InvITs with good liquidity for investing. Managing investment in InvITs is low effort. As you have less choice of investable InvITs, you need not rebalance frequently.

Below table summarizes InvITs as source of passive income.

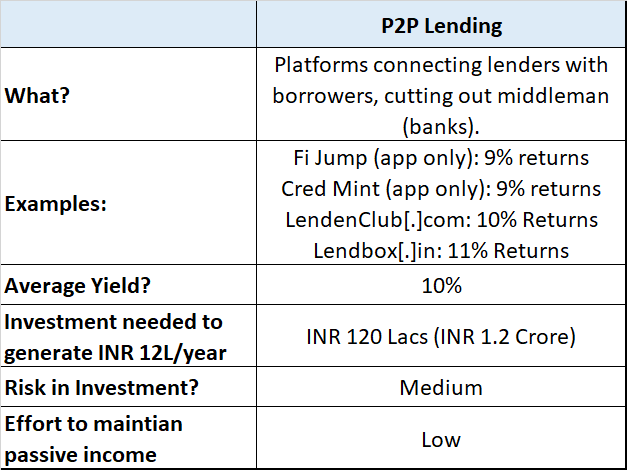

Passive Income 4: P2P Lending

What is P2P Lending?

P2P stands for Peer to Peer. This means one individual lending to another individual. P2P attempts to remove the middleman – the banks – from personal lending chain. Someone who needs money can come on P2P lending platform, and take required loan at slightly cheaper lending rates than what banks would give them. Similarly, individuals with spare money can lend this money on P2P lending platforms, and earn high interest income as compared with savings account interest or fixed deposits’ returns.

Tip: P2P lending is relatively new for the Indian retail investors. P2P lending offers lucrative returns. It is a good idea to try P2P lending by investing small amounts. Once you gain confidence and grow familiar with P2P lending platforms, you can increase your investments.

Average returns from P2P lending

P2P lending, on an average, give you 10% return on invested amount. Once the tenure of P2P lending is complete, you also have your invested capital returned to you. P2P investment returns from some top platforms in India are below.

Fi Jump (app only): 9% returns

Cred Mint (app only): 9% returns

LendenClub[.]com: 10% Returns

Lendbox[.]in: 11% Returns

12% Club (app only): 12% Returns

Investment to generate INR 12Lac/year from P2P lending

Given average annual returns of 10%, we can calculate total investment amount to get INR 12Lac/year income. This will be (INR 12 Lacs)/(10%) = INR 120 Lacs or INR 1.2 Crore.

Risk in P2P Lending

Lending platforms get NBFC P2P license from RBI to become eligible to give P2P loans. This comes with a strong governance and reporting mechanism. Each platform has their checklist to reduce risk among P2P borrowers. Some checks include high CIBIL score, long and consistent debt repayment history etc. P2P platforms also partner with loan aggregators such as Liquiloans to make the process of screening borrowers, and sourcing loans easier.

As P2P lending is a relatively new investment area, there is not much data on defaults which is public. Given this, I will give P2P lending a risk rating of MEDIUM. The reason is that you do not know the borrower, but instead you put trust in the P2P platform to have done due diligence in approving a loan. The second factor is that unlike bonds which have publicly available CARE and ICRA rating, P2P lending does not have these. The third factor is low liquidity. P2P lending requires a minimum lock in of 3 months. If withdrawn in less than 3 months, a small penalty is deducted.

Effort to maintain passive income via P2P lending

As P2P lending requires you to just complete KYC and then invest, it is relatively easy. You do not require to research the borrower, as the P2P platform will do this on your behalf. Hence, the overall effort in P2P lending is LOW. Some P2P lending platforms allow a larger investment horizon of 5 years, so that you can chill and enjoy the passive income for a longer duration.

Below table summarizes P2P Lending as source of passive income.

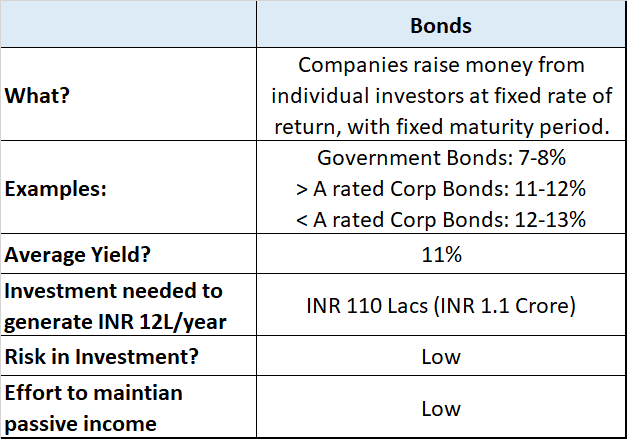

Passive Income 5: Bonds

What are bonds?

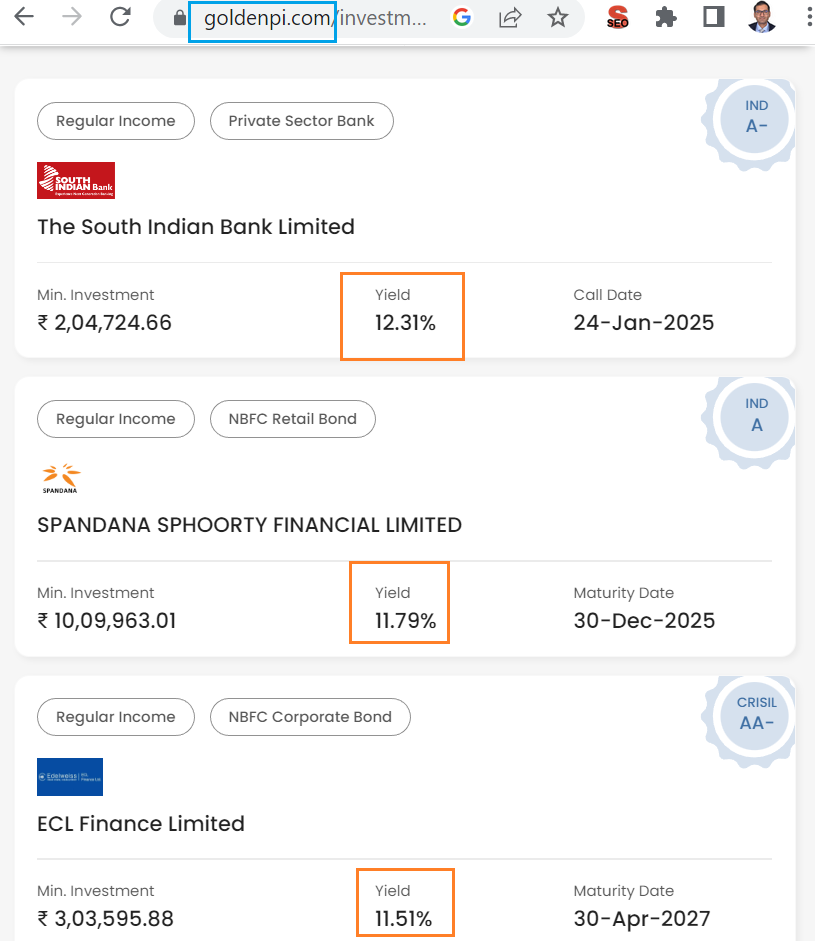

Bonds are one of the oldest methods to generate passive income. Bonds are issued by government or companies or NBFCs. Bond issuer wants to raise funds, and bond holder lends money in return for interest income. Bonds are issued at a fixed rate of return, with a fixed maturity period. One can invest in bonds via bond aggregator platforms such as goldenpi[.]com, wintwealth[.]com. One can also invest in bonds via debt mutual funds. However, debt mutual funds do not distribute regular passive income, hence I will consider individual bond investing in this section.

Average returns from Bond investing

Bonds, on an average give 11% returns. Very safe bonds such as government issued bonds give less returns in the range of 7-8%. Corporate bonds give higher returns of more than 11%. At any point in time, one can find a bond giving more than 11% returns with a credit rating higher than A (refer image below). Hence, I have considered average return of 11% for bond investing. Do note that if you go for bonds with less than A credit rating, you might get 12 or 13% returns as well. However the risk of default will also increase with these lower rated bonds.

Investment to generate INR 12Lac/year from Bonds

We can divide INR 12 Lacs by 11% annual returns to get the investment amount needed. This comes out to (INR 12 Lac)/11% = INR 110 Lacs or INR 1.1 Crore.

Risk in Bonds

Al bonds are issued with a credit rating. The credit rating is given by credit rating agencies such as CARE or ICRA. These credit rating agencies have tight governance and are audited by SEBI regularly. Given this, as long as an investor sticks with a credit rating of A or more, then the risk in bond investing can be considered LOW.

Effort to maintain passive income via Bonds

Bonds have fixed maturity date. This can vary from 1 year to as long as 10 years. Hence, investors do not require to actively manage their bonds’ investments. Once investment is done, one can sit back, and enjoy the monthly bond yield income. Hence, the effort score of bond investing is Low. One does need to review basic details of bonds before investing such as credit rating, the company behind the bond etc. But once invested, one need not track or rebalance their bond investment frequently.

Below table summarizes Bonds as source of passive income.

Additional Points to Note for Passive Income methods

We saw that investing in more than A rated corporate bonds give the highest passive income. If you have INR 1 crore, should you invest in bonds and chill the rest of your life? Well not so fast. Theoretically you can do this. However do keep below points in minds.

Note 1: Taxes

Taxes dampen every party, and passive income party is no different. You need to be smart about taxes, and take tax exemptions wherever applicable. Using ELSS funds, PPF, NPS, Health Insurance, you can easily waive off INR 2.5 lac yearly income from taxes. This will make your taxable passive income of INR 12 Lac as INR 9.5 Lac, which will attract 20% income tax. I will not go deep into saving taxes in this post, but you should evaluate tax impact for yourself.

One good point to note is that except dividend income, all other passive income such as P2P lending income, bond interest income will come without TDS (Tax Deducted At Source) deduction. This means that you can enjoy the full INR 12 Lac passive income for the year, and pay taxes only at the end of the year!

Note 2: What about dependents?

This post takes into account an individual person. I have assumed for one person, INR 12Lac per year is more than sufficient. But this amount can vary on your lifestyle. If you move to a Tier 2 city, your annual expenses will reduce by as much as 20%, and INR 10Lac/year should suffice for your needs.

If you have dependents such as retired parents, or kids, then your total passive income requirements will go up. Still, getting a good passive income will give you the confidence to pursue your passion, and take risk head on.

Note 3: But I don’t have INR 1 Crore??

Yes, no one has INR 1 Crore lying in their bank account. That is where planning comes in. Plan your savings and investments to get to the point where you can live off your passive income. This planning can take you 5 years, or 7 years, depending on your income, lifestyle etc. This post is aimed to show that financial freedom is possible. Once you have seen the rosy picture beyond financial freedom, I hope you will be more motivated to reach to that point.

Sumamry

Summarizing, my favorite method of generating passive income is bonds. Below table compares all 5 methods to generate passive income for a quick reference.

Hope this post helped you become aware of five methods to generate passive income. Financial freedom is no longer aspiration, but a realistic milestone. Many individuals are taking this route to unlock their true calling. Even if you are satisfied with your job and life, getting some passive income does sweeten your day.

Which passive income do you prefer, and why? Comment below.

Happy Investing!