What is the fuss?

Fixed Deposit (FD) is a boring way of investing your money. FD provide a fixed interest rate on the principal amount you invest. The investment is for a fixed period, starting from 1 year to 5 years or more. Fixed interest rates, and fixed tenure of investment is probably why ‘Fixed Deposit’ get its name. The fixed parts definitely give FDs a boring air around them.

FDs, in recent years, have received less love from social media influencers. The broader message circulating is that FDs do not even beat inflation, and hence reduce your wealth over time. Well, part of this is not true. In this post I will tell you three lesser known reasons why you need a Fixed Deposit as a part of your investment portfolio. Lets get started, bust some myths, and know some interesting facts & uses of FDs.

Why is there negative sentiment around FDs?

The main reason behind negative sentiment surrounding FDs is inflation. Beating inflation is essential. If not done, your wealth will reduce over time.

Now, gains made from FDs are fully taxed as per your income tax bracket. These taxes decrease the net gains made by the investor. Unlike equity investment, where long term capital gains tax rate is just 10%, gains made from FDs are charged fully as per your income tax slab, irrespective of the period of investment.

Now, there is a catch. Social media influencers, who advise not to invest in FDs, often use common public and private banks’ FDs as examples. Most of these banks offer Fixed Deposit interest rates in the range of 6–7%. Now, this does not even beat inflation, which stands at 7.4% in September 2023 as I write this post. And they are correct, investing in these FDs will not even beat inflation. So, do not invest in FD offered by big banks such as SBI, HDFC, ICICI etc.

Now, the next obvious question is, are there FDs which beat inflation, and offer more than 8% interest rate? The answer is yes. I cover this in the following section.

Lets look at four reasons why you absolutely need a Fixed Deposit as part of your investment portfolio. Lets start with reason 1 — beating inflation.

[Reason 1] You need FD to beat inflation

Yes, you read it right, FDs can beat inflation too.

To understand how, one needs to understands why are FDs provided to retail investors like us. Fixed Deposit is provided by financial institutions because they need to raise funds. Why do these financial institutions need to raise funds? To lend money to others, such as corporates, home loans, student education loan etc. Why do financial institutions lend money? Well, to make money.

The main source of income of almost all financial institution is lending money. The reason is because lending offers the highest rates of interest these institution can charge. The net interest income of these institutions is (Lending Interest rate) — (Borrowing interest rate). Borrowing interest rate is also called the cost of funds. Cost of funds is the interest rate these financial institutions pay to retail investors like us from whom they borrow money.

Example: A Home loan interest rate is 12%. And FD interest rate to depositors is 6%. then the financial institution makes a net interest income of (12–6)%, or 2%.

Now, it is obvious that any company tries to maximise its profits. Big banks already have a low source of funds — savings bank account. Interest rate given on savings bank account is a meagre 3%. Hence, these large banks are not incentivised to give higher interest rate on Fixed Deposits.

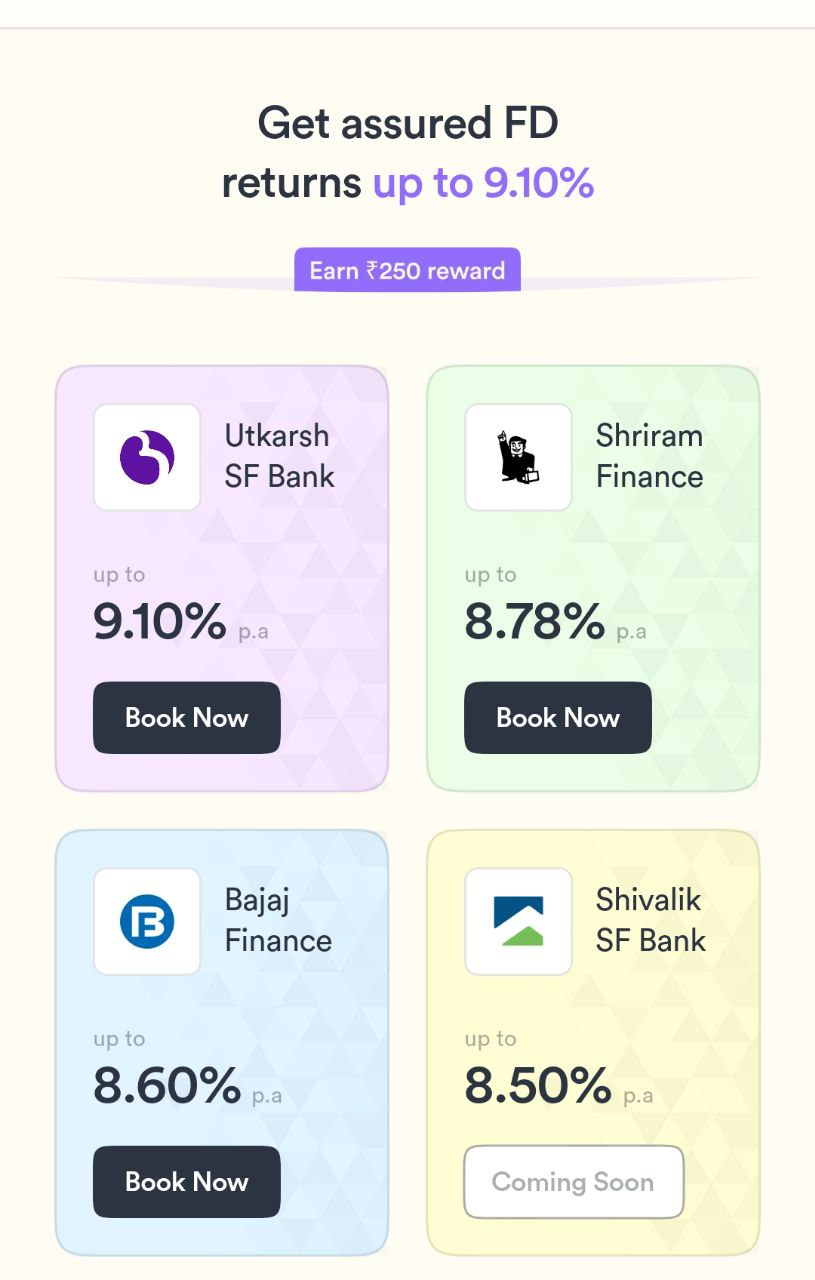

But, what about other financial institutions? I am talking about NBFCs (Non Banking Financial Institutions) who do not enjoy low source of funds such as savings bank accounts. These NBFCs offer higher FD interest rates to attract retail investors. Some notable NBFCs offering high FD interest rates are:

Bajaj Finance — FD rate of upto 8.60%

Shriram Finance — FD rate of upto 8.78%

Small banks, who are in dire need of funds to lend, also offer higher FD interest rates.

Many small finance banks offer more than 8.5% annual interest on Fixed Deposits. Some notable ones are AU Small Finance Bank, Ujjivan Small Finance Bank, Utkarsh Small Finance Bank, and Suryodaya Small Finance Bank. Also note that for senior citizens (age > 60 years), all these banks offer an additional 0.5% interest. Which means that for senior citizens all these small finance banks offer north of 9% annual interest rate. Even if you are not in a senior citizen yet, you can invest in the name of a senior citizen in your family to avail the higher interest rates.

So, now you know some financial institutions who offer higher than inflation FD interest rates. What is more interesting, is the concept of locking in a FD rate. What this means is that if you open a FD for 5 years, and lock in an interest rate, the interest rate will get locked in for the entire 5 years. If in that 5 years, the overall banks’ lending rate drops, it will not impact your FD returs as its rate is locked for 5 years. It is best to lock in a long term FD interest rate when FD rates are at the highest. FD rates are usually at their highest just after a high inflationary environment, like we see in 2023.

Do note that a Fixed Deposit is not the best wealth compounding machine. But if played well, it can definitely beat inflation, and preserve your wealth. And that is what it should be used for.

Now, as you feel comfortable on beating inflation, lets look at two additional lesser known reason I use FD.

[Reason 2] You need FD for short term liquidity

You need liquidity. Any emergency can turn up. An unexpected tooth’s root canal treatment. An urgent flight booking to cater to a family emergency. Or a sudden ask by your owner to vacate your rental apartment — ouch!

There is another reason why many active retail investors like me keep liquid money. In the world of equity investment, you make money by buying low and selling high. For this, you need to wait and accumulate money during phases when the stock market is expensive. And when the market corrects or falls, you deploy your accumulated money into the stock market. Once deployed, as the market recovers and reaches new highs, you make money. This is a time tested way to make money. However, you need a good way to store money, in a very liquid form.

Now, there are several ways to store your money in a liquid form. Below are some ways. And, as you will find out soon, FDs are the best liquid forms of storing emergency money.

Savings Banks Account

These give very low returns (3% annually). They are highly liquid. You can directly pay using your savings account using UPI, IMPS etc. payment modes.

Liquid Mutual Funds

They give average returns, in the range of 4 to 5% annually. Their liquidity is just about average as well. You can place a withdrawal order alright, but the money will hit your bank account in 3–4 working days. So it is not immediately available for use.

Do note that investment instruments such as P2P lending, T-Bills issued by RBI etc. are not liquid. These come with a lock-in period. Hence I am not considering these instruments for storing money for short term liquidity.

Now, comes FD.

Fixed Deposits

As we have seen FDs give high interest rates of upto 9% annually. They are highly liquid as well. You can break your FD in a matter of seconds, withdrawing your money to your bank account. You do have to pay a minor penalty for early withdrawal, which is usually 1% of overall interest earned on the FD. Even with this early withdrawal fee, you will get higher returns from using FD vs a short-term liquid money source.

There you go, FDs are super helpful to keep liquid money, be it for emergency needs. Some people, including me, park at least 6–8 months of lifestyle expensed in FDs as well. In this predictable world, who knows when we may lose our jobs, and miss the monthly ‘salary credited SMS’. In these situations, breaking FD is better than withdrawing money from equities. The latter may negatively impact your wealth compounding.

[Reason 3] You need FD for low risk investment

FDs have very low risk. Almost close to zero risk. But probably you already knew that. Investment in FDs has been a knowledge passed on across generations in India. However, it is important to understand why FDs have low risk, to help you declutter the investment options available to the modern retail investor. Here we go.

You might have come across many investment options such as P2P lending, which offer annual returns as high as 12%. But the catch is the promise made, it says ‘upto’, and not just 12%. There is the catch. Investment options such as P2P lending do not guarantee the said return. The mentioned return might be the highest possible return, but the net return will mostly be averaged down. But that is not the case with FD returns. The interest rate that you lock in an FD, is what you get. No questions asked.

The reason why FD rates are fixed, because banks and NBFCs in turn lend the money out at fixed rates. In case the borrower defaults, banks and NBFCs have other ways of recuperating that loss. These financial institutions will make good of the promised interest rate to depositors like us.

The second, lesser known reason of low risk in FDs, is insurance. Yes, you read it right. RBI insures all FDs (principal as well as interest earned) upto INR 5 Lacs. And as a depositor, you do not have to pay a single penny to get this insurance. All FD investors are by default eligible under this insurance. Isn’t that cool?

Parting Thoughts

FD is an investment instrument which carries low risk, is highly liquid, and beats inflation if chosen right. FD give you peaceful sleep at night, as they are not volatile like the stock market. FDs should be one of the core pillars of your investment portfolio.

The question that may be popping in your head is, what percentage allocation of your wealth should be done in FDs? Well, this is for each of you to answer. Definitely, a large allocation should go into equities, which compound your wealth. Your FD allocation should depend on the size of your emergency fund (6–8 months of lifestyle expense), and the size of cash you want to accumulate to deploy later in other investment assets such as equities or real estate etc.

I personally like Stablemoney to do FD investments. They are an app which acts as FD aggregator across leading banks and NBFCs.

Hope you now know some of the lesser known reasons why you need FDs in your portfolio.

Do you have a FD? If yes, in which bank/NBFC, and what is the FD interest rate you get? Do share in the comments below.

Pingback: 2 things Banks and NBFCs don’t want you to know about Fixed Deposits - Mayank Dwivedi